Michael (Xiaochen) Sun

Director, Quant Capability,

Client Portfolio Manager,

Quantitative Strategies,

Eastspring Investments

Aug 2025|5 min read

Executive Summary

- Defensive investing, much like football defence, is crucial for long-term success. Just as defenders anchor a football team, low-volatility strategies provide portfolio stability and resilience amid market uncertainty.

- Market volatility, driven by multiple exogenous shocks, and rising concentration in Asian equity markets highlight the need for diversification. With fewer effective stocks in multiple markets, active management and systematic low-volatility approaches offer a strategic edge.

- History shows that an Asian-focused low-volatility strategy has consistently outperformed the broader market in turbulent and moderately bullish markets, making them a reliable choice for navigating volatile markets.

“Attack wins you games, defence wins you titles” – Sir Alex Ferguson1.

With Premier League clubs currently playing their pre-season fixtures across Asia, the importance of an effective defence can be seen in full play. Whatever a football team’s formation, be it 4-4-2, 4-2-3-1, 3-4-3 or any other setup, every successful strategy includes defenders. Defenders provide stability, shielding against turbulence and unexpected threats and ensuring the team remains effective under pressure. In much the same way, a defensive investment allocation, such as in a systematic low-volatility strategy, acts as the anchor of a portfolio, offering resilience across a wide range of market conditions.

A messy pitch

We have gone past half time, and global equity markets have navigated a turbulent seven months of the year, characterised by alternating risk-on and risk-off sentiment. The period was shaped by tariff uncertainties and subsequent deals/extensions, policy developments such as the "One Big Beautiful Bill Act", geopolitical tensions in the Middle East, and a better-than-expected US corporate earnings season. More recently, signs of cracks in the US labour market and President Trump’s tariff announcements caused the S&P 500 to fall 1.6% on 1 August, the most negative since May 2025.

Uncertainty remains a central theme in global markets. Uncertainty persists around policy direction, the outcome of trade tariffs, and the trajectory of economic growth.

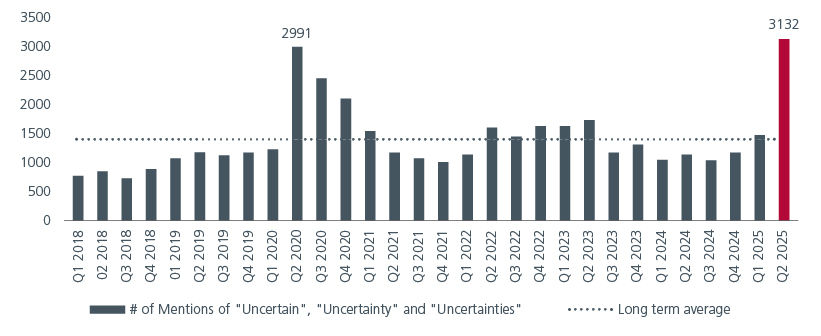

While US corporate earnings have been strong, data suggests that this uncertainty is now filtering through to earnings. Since the beginning of April, the terms “uncertain,” “uncertainty,” and “uncertainties” have appeared approximately 3,100 times in corporate earnings calls, conference presentations and related events, according to transcript analysis compiled by Bloomberg. This marks the highest quarterly count in over two decades, surpassing even the peaks seen during the Global Financial Crisis in 2008 and the onset of the Covid-19 pandemic in 2020. Clearly, the level of uncertainty continues to rise.

Fig. 1. No. of mentions of “uncertain”, “uncertainty” and “uncertainties”

Source: Bloomberg. Note: Data through close of trading on 29 May. Includes transcripts of earnings calls, conference presentations and other events.

Against this backdrop, Asian and Emerging Market (EM) equities have outperformed US and developed market equities. With the Dollar Index down 9% year to date, a trend that is historically supportive of EM assets and expected to continue, Asia and EMs’ attractive valuations look compelling. This positions them well to attract capital seeking diversification from US-centric portfolios.

Playing active defence

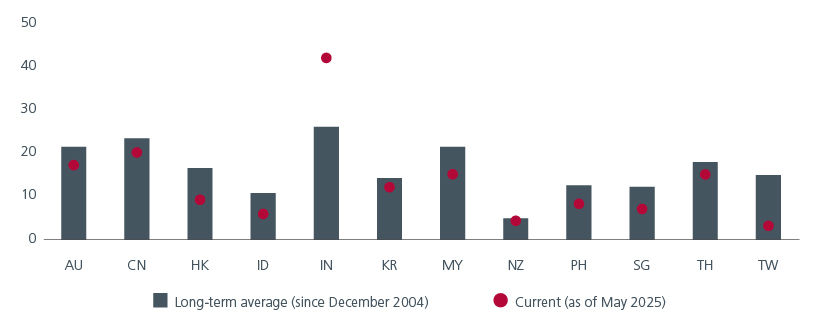

Amid the volatility, Asian markets are becoming increasingly concentrated, with the effective number of stocks in Asia Pacific ex-Japan now well below their long-term average. The “effective number of stocks” helps us to understand how diversified a market index is. It is calculated as the inverse of the Herfindahl-Hirschman Index (HHI), a commonly used measure of concentration. The higher the HHI, the lower the effective number, the more concentrated the market index. See Fig. 2. Taiwan in particular stands out with just three effective stocks. This growing concentration highlights the pressing need for diversification and reinforces the value of active management in Asia.

Fig. 2. Effective number of stocks

Source: Eastspring Investments and MSCI. As of 30 May 2025.

As such, for investors with existing exposures in Asian equities or looking to increase their allocations, a systematic low-volatility strategy appears well suited given the current market volatility. Rather than chasing short-term fads which could lead to over-concentration in portfolios, a systematic low-volatility strategy is based on a long-term investment thesis which is grounded on the statistical average of sound investment principles, specifically, the low-volatility anomaly. This anomaly, coupled with refinements introduced by practitioners, suggests that stocks with lower price fluctuations, attractive dividend yields, and multi-factor alpha characteristics tend to deliver superior risk-adjusted returns over time.

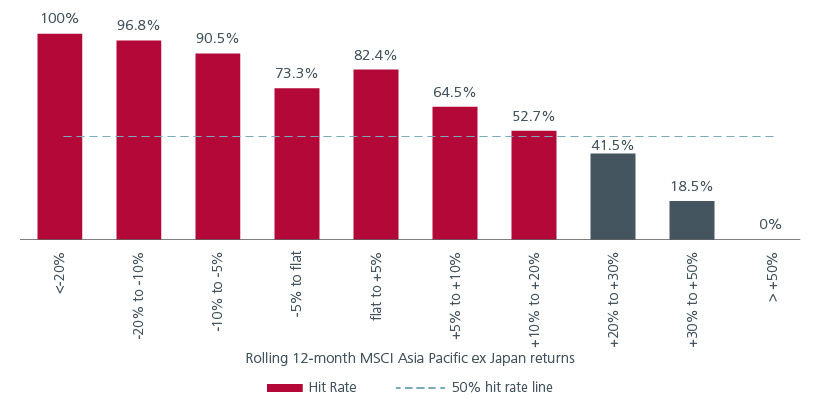

Historical data over more than 24 years supports this – the rolling 12-month returns of an Asian-focused low-volatility strategy, proxied by the MSCI AC Asia Pacific ex-Japan Minimum Volatility Index, have consistently outperformed the broader market during periods of market stress, as well as during periods of modest or steady gains. This performance holds across diverse market scenarios, from declines of -20% to gains of +20%. Notably, the low-volatility style has a greater than 50% probability of outperforming the broader market when the market’s returns range between +10% and +20%, demonstrating the strategy’s robustness even in moderately bullish environments. Fig. 3. illustrates this dynamic clearly.

Fig. 3. Hit rate of low-volatility strategy beating the market

Source: Eastspring Investments, MSCI. As of 31st July 2025. MSCI AC Asia Pacific ex Japan Minimum Volatility Index used as a proxy for low-volatility strategy. Please note that there are limitations to the use of such indices as proxies for the past performance in the respective asset classes/sector. The chart above is included for illustrative purposes only and may not be indicative of the future or likely performance of the markets

Scoring with stability

While year-to-date equity market rallies have been narrow, and skewed towards high-growth, high-volatility stocks, the recent market sell-off in early August and the potential for a period of range-bound trading, highlights the enduring importance of defensive allocations in investor portfolios. Just as defenders in football teams are key in securing victories, low volatility strategies play a vital role in helping portfolios weather market turbulence by mitigating downside and delivering consistent returns over time.

Interesting reads

Sources:

1 the legendary former manager of Manchester United.

This document is produced by Eastspring Investments (Singapore) Limited and issued in:

Singapore by Eastspring Investments (Singapore) Limited (UEN: 199407631H)

Australia (for wholesale clients only) by Eastspring Investments (Singapore) Limited (UEN: 199407631H), which is incorporated in Singapore, is exempt from the requirement to hold an Australian financial services licence and is licensed and regulated by the Monetary Authority of Singapore under Singapore laws which differ from Australian laws

Hong Kong by Eastspring Investments (Hong Kong) Limited and has not been reviewed by the Securities and Futures Commission of Hong Kong.

Indonesia by PT Eastspring Investments Indonesia, an investment manager that is licensed, registered and supervised by the Indonesia Financial Services Authority (OJK).

Malaysia by Eastspring Investments Berhad (200001028634/ 531241-U) and Eastspring Al-Wara’ Investments Berhad (200901017585 / 860682-K) and has not been reviewed by Securities Commission of Malaysia.

Thailand by Eastspring Asset Management (Thailand) Co., Ltd.

United States of America (for institutional clients only) by Eastspring Investments (Singapore) Limited (UEN: 199407631H), which is incorporated in Singapore and is registered with the U.S Securities and Exchange Commission as a registered investment adviser.

European Economic Area (for professional clients only) and Switzerland (for qualified investors only) by Eastspring Investments (Luxembourg) S.A., 26, Boulevard Royal, 2449 Luxembourg, Grand-Duchy of Luxembourg, registered with the Registre de Commerce et des Sociétés (Luxembourg), Register No B 173737.

Chile (for institutional clients only) by Eastspring Investments (Singapore) Limited (UEN: 199407631H), which is incorporated in Singapore and is licensed and regulated by the Monetary Authority of Singapore under Singapore laws which differ from Chilean laws.

The afore-mentioned entities are hereinafter collectively referred to as Eastspring Investments.

The views and opinions contained herein are those of the author, and may not necessarily represent views expressed or reflected in other Eastspring Investments’ communications. This document is solely for information purposes and does not have any regard to the specific investment objective, financial situation and/or particular needs of any specific persons who may receive this document. This document is not intended as an offer, a solicitation of offer or a recommendation, to deal in shares of securities or any financial instruments. It may not be published, circulated, reproduced or distributed without the prior written consent of Eastspring Investments. Reliance upon information in this document is at the sole discretion of the reader. Please carefully study the related information and/or consult your own professional adviser before investing.

Investment involves risks. Past performance of and the predictions, projections, or forecasts on the economy, securities markets or the economic trends of the markets are not necessarily indicative of the future or likely performance of Eastspring Investments or any of the funds managed by Eastspring Investments.

Information herein is believed to be reliable at time of publication. Data from third party sources may have been used in the preparation of this material and Eastspring Investments has not independently verified, validated or audited such data. Where lawfully permitted, Eastspring Investments does not warrant its completeness or accuracy and is not responsible for error of facts or opinion nor shall be liable for damages arising out of any person’s reliance upon this information. Any opinion or estimate contained in this document may subject to change without notice.

Eastspring Investments companies (excluding joint venture companies) are ultimately wholly owned/indirect subsidiaries of Prudential plc of the United Kingdom. Eastspring Investments companies (including joint venture companies) and Prudential plc are not affiliated in any manner with Prudential Financial, Inc., a company whose principal place of business is in the United States of America or with the Prudential Assurance Company Limited, a subsidiary of M&G plc (a company incorporated in the United Kingdom).