Eastspring Investments

May 2023 | 5 min read

Summary

Asia is transforming. To stay relevant, global chief executives acknowledge that their business models must evolve to cater to the region’s emerging market trends. As companies reinvent, new business ideas are likely to translate to new investment opportunities.

Many businesses are turning to Asia for growth and transformation opportunities. The region’s improved technological capabilities and infrastructure, growing innovation and an expanding consumer class, offer possibilities that are unparalleled elsewhere. In our whitepaper “Asia 2.0: Investing in an era of new opportunities”, we surveyed 100 C-suite global business leaders across multiple industries for their insights on the region’s unique opportunities and challenges to expansion.

Based on the survey, more than two-thirds of business leaders believe that India holds the most potential for expansion or transformation opportunities, followed by China and Indonesia. All three have large consumer markets with India and Indonesia offering a boost from their growing middle-class populations. Meanwhile China’s leading role in electric vehicle manufacturing and renewable energy will allow investors to capitalise on Asia’s green transition.

Unique consumer opportunities

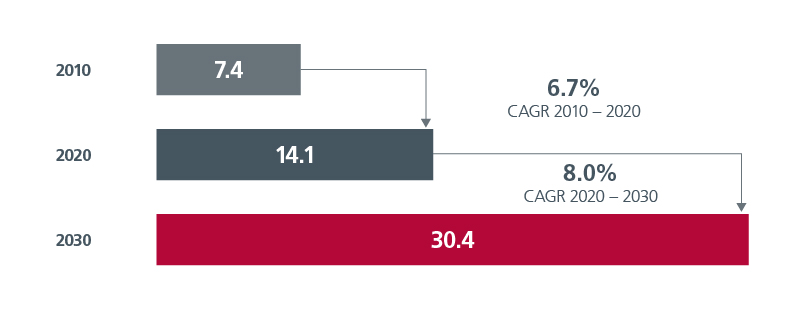

Presently, Asia is home to 55% of the global consumer class. Over the next decade, Asian countries will continue to be the world’s fastest growing consumer markets. By 2030, India, China and Indonesia will jointly add over 830 million consumers.1 As the expanding populations and rising income levels fuel greater demand, consumer spending too will grow at a faster rate, reaching USD30.4 trillion by 2030.

Fig 1: Consumer expenditure in Asia, USD trillion

Source: Euromonitor, 1 March 2023

77% of the business leaders surveyed cite the region’s growing and evolving consumer base as one of the key reasons they are looking to Asia for expansion opportunities. They also highlighted the unique opportunities they see in Asia arising from this trend.

One among these is the growing high-net-worth individuals (HNWIs) in Asia. Between 2021 to 2026, the population of HNWIs in Asia Pacific is forecasted to grow by 59.8%. According to Knight Frank’s wealth report, Asia-Pacific will be the largest regional wealth hub by 2026.2 This trend will have long lasting investment implications for the property, healthcare and consumer discretionary sectors as wealthier individuals demand better quality of products and services.

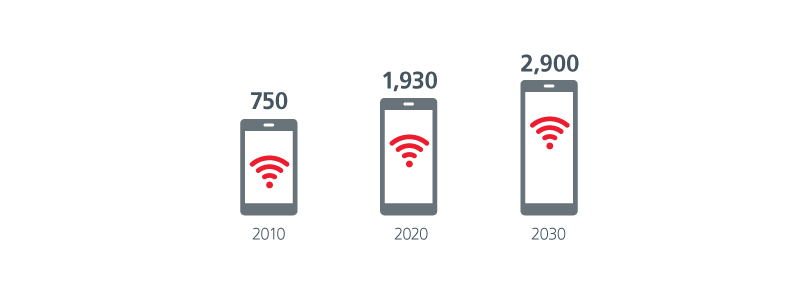

Next is Asia’s rapidly increasing internet penetration arising from the region’s high smart phone penetration rates and mobile-savvy populations. It is estimated that 60 million people in Southeast Asia became online consumers during the pandemic. 3 The rise in mobile and live streaming e-commerce is expected to generate new channels of consumption and opportunities.

Fig 2: Internet users in key Asian markets4, millions

Source: Euromonitor, 24 February 2023

Others see Asia playing a leading role in the world’s transition to net zero. Countries’ zero-carbon targets, better charging infrastructure as well as cheaper and more efficient batteries will increase electric vehicle (EV) adoption going forward. By 2030, key economies in Asia are expected to account for 52% of global passenger EV sales.5

Key expansion enablers

Business leaders however are cognisant that Asia’s next transformation will have to be supported by key enablers. 62% indicate better physical and digital infrastructure, 56% specify the increasingly educated and skilled workforce, 52% mention the improving business operating environment and 50% note the supportive government policies.

Asia has made vast improvements in its physical and digital infrastructure. For example, more is being done to upgrade the technology infrastructure (wireless networks, data centres, etc.) to cater to Asia’s growing numbers of internet users. Between 2022 and 2025, mobile operators in Asia Pacific are set to invest around USD227 billion in 5G deployments. Improved connectivity has also facilitated India’s digital adoption, by tapping into the dormant potential of its increasingly affluent, rural population.

The profile of the region’s labour market is changing with the workforce becoming more educated and skilled. According to the 2021 Times Higher Education World University Rankings, nearly one-third of top 200 universities are based in Asia, compared to 26% in 2016. 44% of the business leaders in the survey plan to invest in talent and leadership development over the next 2 to 3 years. The emphasis on digital skills can pave the way for Asia to become a regional hub for skilled talent.

Meanwhile governments have introduced several policies to improve the overall business environment to encourage expansion and foreign direct investments into the region. These include labour and tax reforms, reduced business operating costs and relaxed requirements for IPO listings. Incentives for greater private sector participation should also bolster the region’s attractiveness. Given this, 64% of the business leaders look to forge new partnerships/joint ventures to increase market presence in Asia.

Challenges to expansion

While Asia’s growth potential is undeniable, there are challenges too. 56% of the survey respondents picked geopolitical uncertainty as a key risk, mainly the growing tensions between US and China. Meanwhile 55% concurred that expanding in Asia meant facing regulatory constraints and complex legal frameworks. Asia’s heterogeneity means that markets have differing political regimes, regulatory requirements, intellectual property rights and data protection laws, which can oftentimes be difficult to navigate.

Separately, nearly 50% of survey respondents are worried that inflation and high interest rates will exacerbate economic uncertainty. In any case inflation is less of an issue in Emerging Asia relative to Developed Markets. Asian central banks too typically tend to be more growth focused; the Monetary Authority of Singapore, for example, paused on the monetary policy tightening in April amidst signs of a slowing economy.

Asia is also highly susceptible to climate change risks and natural disasters. Between 2000 and 2019, 37% of all weather-related disasters occurred in Asia Pacific – the highest globally. Given more pronounced and frequent climate disasters, about one-third of the respondents acknowledged that ESG-related challenges pose as one of the risks.

Fig 3: Specific ESG risks identified by business leaders

Source: Eastspring Investments’ whitepaper: Asia 2.0: Investing in an era of new opportunities, 11 May 2023

What’s in it for investors?

As businesses restructure their footprint, consumer trends are also seeing a shift. 53% of businesses are launching new products and services to adapt to Asia’s evolving consumer class. With higher incomes, demand for quality products have increased. Consumers are more conscious about health and food safety, as well as ESG. These dovetail to drive demand for new food products, such as plant-based alternatives. In addition, high mobile internet penetration across Asia will drive demand for online products and services – such as digital banking, mobile wallets, Buy-Now-Pay-Later (BNPL) and insurtech products. Companies that embrace these emerging trends will be likely beneficiaries.

All said, to succeed in a diverse region like Asia, businesses require an understanding of local market conditions and an ability to navigate complex regulatory and legal frameworks. Similarly, to reap significant alpha from the region, investors should adopt an active investment approach to identify the winners.

Interesting reads

Sources:

1 https://www.statista.com/chart/25990/consumer-markets-growth/

2 https://www.knightfrank.com/research/article/2022-07-21-the-wealth-report-2022-10-key-highlights-pertaining-to-the-asiapacific-landscape

3 Nikkei Asia. COVID’s striking impact on Southeast Asia’s digital economy. November 2021.

4 Key markets include China, Hong Kong, India, Indonesia, Japan, Malaysia, Singapore, South Korea, Taiwan, Thailand, and Vietnam

5 Data for Taiwan and Vietnam not available

Singapore by Eastspring Investments (Singapore) Limited (UEN: 199407631H)

Australia (for wholesale clients only) by Eastspring Investments (Singapore) Limited (UEN: 199407631H), which is incorporated in Singapore, is exempt from the requirement to hold an Australian financial services licence and is licensed and regulated by the Monetary Authority of Singapore under Singapore laws which differ from Australian laws

Hong Kong by Eastspring Investments (Hong Kong) Limited and has not been reviewed by the Securities and Futures Commission of Hong Kong.

Indonesia by PT Eastspring Investments Indonesia, an investment manager that is licensed, registered and supervised by the Indonesia Financial Services Authority (OJK).

Malaysia by Eastspring Investments Berhad (200001028634/ 531241-U) and Eastspring Al-Wara’ Investments Berhad (200901017585 / 860682-K) and has not been reviewed by Securities Commission of Malaysia.

Thailand by Eastspring Asset Management (Thailand) Co., Ltd.

United States of America (for institutional clients only) by Eastspring Investments (Singapore) Limited (UEN: 199407631H), which is incorporated in Singapore and is registered with the U.S Securities and Exchange Commission as a registered investment adviser.

European Economic Area (for professional clients only) and Switzerland (for qualified investors only) by Eastspring Investments (Luxembourg) S.A., 26, Boulevard Royal, 2449 Luxembourg, Grand-Duchy of Luxembourg, registered with the Registre de Commerce et des Sociétés (Luxembourg), Register No B 173737.

Chile (for institutional clients only) by Eastspring Investments (Singapore) Limited (UEN: 199407631H), which is incorporated in Singapore and is licensed and regulated by the Monetary Authority of Singapore under Singapore laws which differ from Chilean laws.

The afore-mentioned entities are hereinafter collectively referred to as Eastspring Investments.

The views and opinions contained herein are those of the author, and may not necessarily represent views expressed or reflected in other Eastspring Investments’ communications. This document is solely for information purposes and does not have any regard to the specific investment objective, financial situation and/or particular needs of any specific persons who may receive this document. This document is not intended as an offer, a solicitation of offer or a recommendation, to deal in shares of securities or any financial instruments. It may not be published, circulated, reproduced or distributed without the prior written consent of Eastspring Investments. Reliance upon information in this document is at the sole discretion of the reader. Please carefully study the related information and/or consult your own professional adviser before investing.

Investment involves risks. Past performance of and the predictions, projections, or forecasts on the economy, securities markets or the economic trends of the markets are not necessarily indicative of the future or likely performance of Eastspring Investments or any of the funds managed by Eastspring Investments.

Information herein is believed to be reliable at time of publication. Data from third party sources may have been used in the preparation of this material and Eastspring Investments has not independently verified, validated or audited such data. Where lawfully permitted, Eastspring Investments does not warrant its completeness or accuracy and is not responsible for error of facts or opinion nor shall be liable for damages arising out of any person’s reliance upon this information. Any opinion or estimate contained in this document may subject to change without notice.

Eastspring Investments companies (excluding joint venture companies) are ultimately wholly owned/indirect subsidiaries of Prudential plc of the United Kingdom. Eastspring Investments companies (including joint venture companies) and Prudential plc are not affiliated in any manner with Prudential Financial, Inc., a company whose principal place of business is in the United States of America or with the Prudential Assurance Company Limited, a subsidiary of M&G plc (a company incorporated in the United Kingdom).