Summary

Following the 20th Party Congress, investors should look out for the specific growth targets and policies that will be set out in the upcoming Central Economic Work Conference in December and the National People’s Congress in March next year. We believe that there will be increasing policy support towards self-sufficiency, energy safety and technology independency and will look for investment opportunities in related sectors.

China’s 20th Party Congress ended over the weekend with President Xi securing a third term as the chairman of the Communist Party. Changes were also made to the Politburo Standing Committee with four newly appointed members (Li Qiang, Cai Qi, Ding Xuexiang and Li Xi). They replace Li Keqiang (Premier of the State Council), Li Zhanshu (Chairman of the Standing Committee of the National People’s Congress), Wang Yang (Chairman of the National Committee of the Chinese People’s Political Consultative Conference) and Han Zheng (Vice Premier of the State Council) who will all retire from their current posts. It is widely expected that Li Qiang (Current Party Secretary of Shanghai) will replace Li Keqiang as the Premier of the State Council. This will only be confirmed and announced in March next year, when China holds its National People’s Congress.

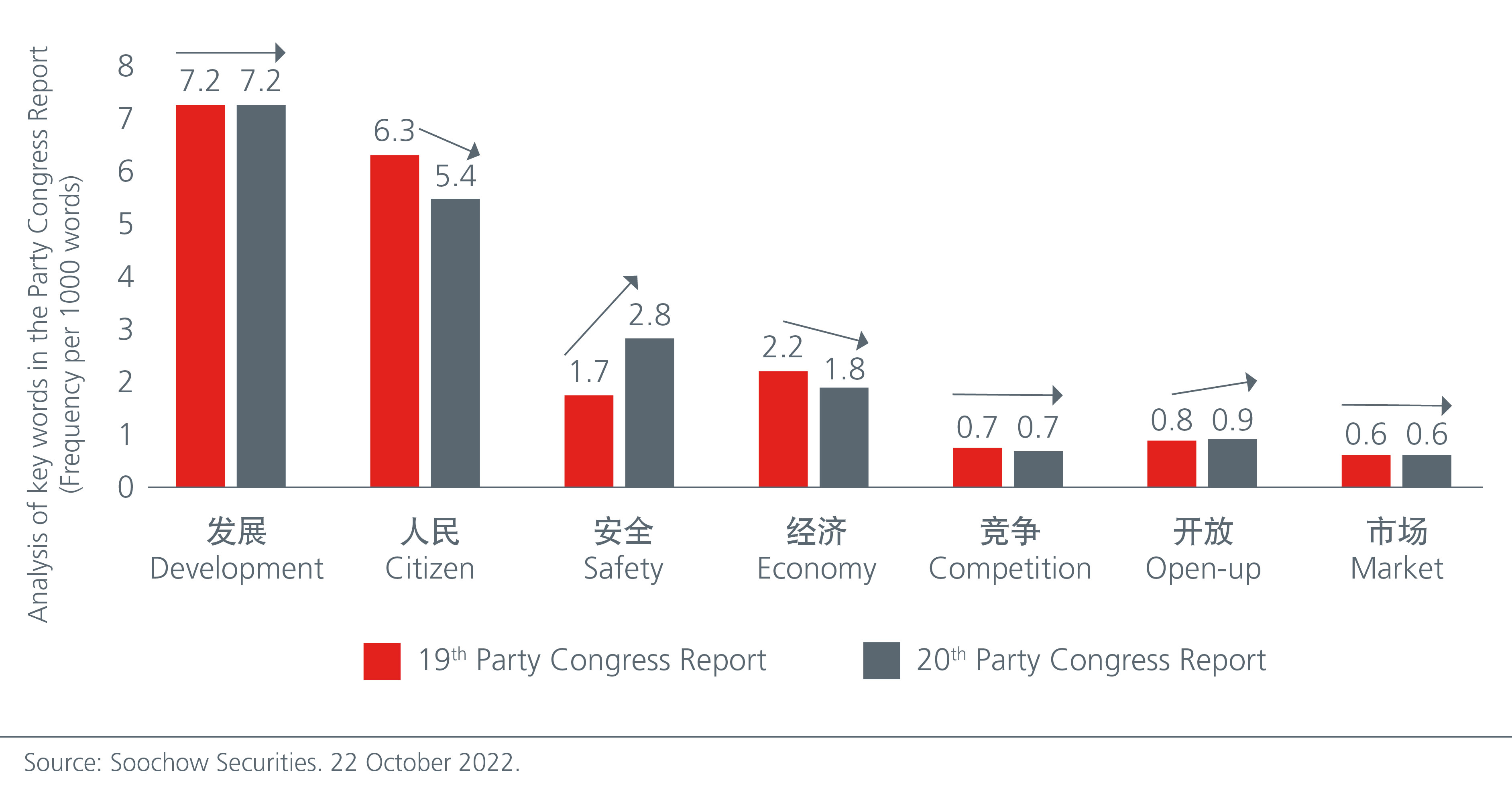

The make-up of the Politburo Standing Committee reflects a centralised decision-making process which may disappoint markets in the near term. President Xi’s Work Report (“Report”) focused on keywords such as “development”, “people” and “safety” (See Fig. 1) but did not drop the words “market” and “opening up” which was a key concern among investors before the meeting. Importantly, the Report indicated that the Communist Party of China (“CPC”) will continue its reforms towards a “socialist market economy”, and “promote high-quality development”.

Fig. 1. Analysis of key words in the Party Congress Report (Frequency per 1000 words)

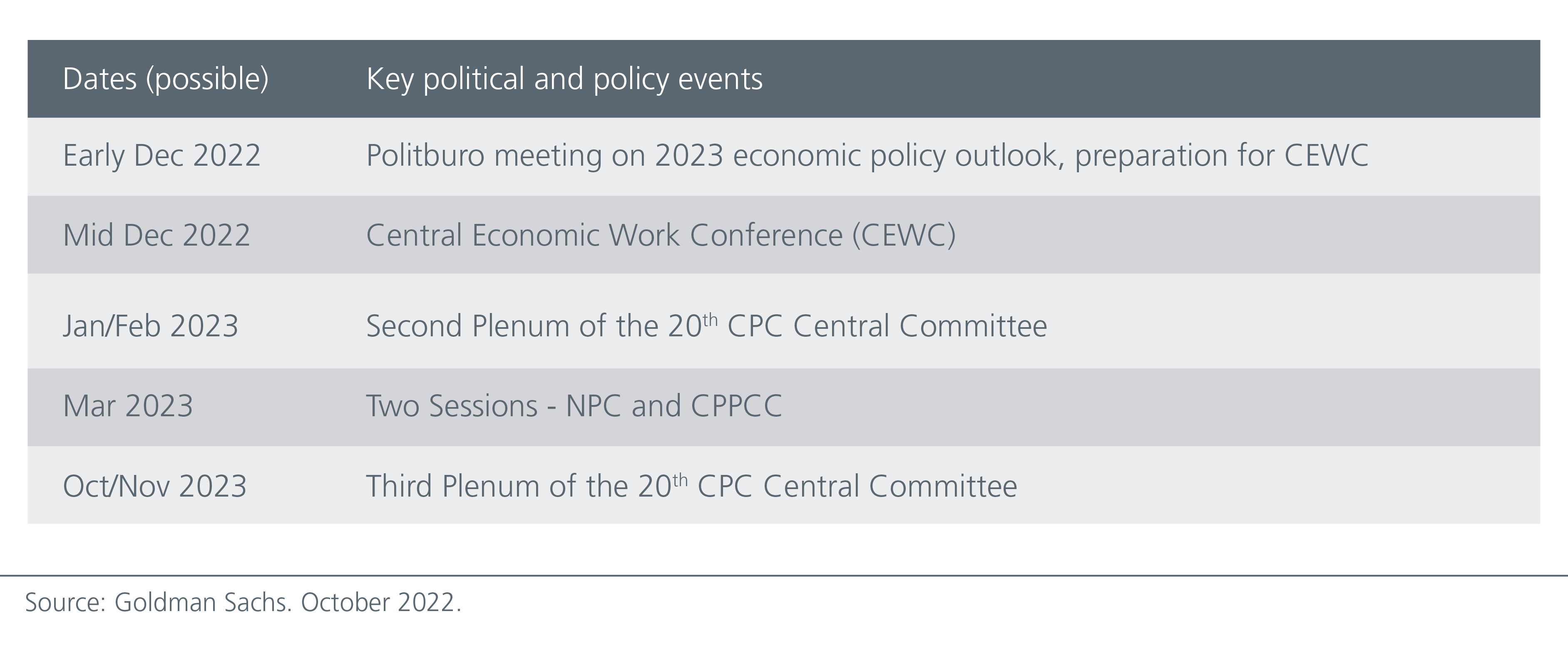

For investors who may view “development” as a vague concept and were hoping for specific growth targets, it is worth noting that the Party Congress convenes every five years and typically focuses on the long-term vision and objectives of the CPC for the country. Shorter-term economic policies and targets will be unveiled in the Central Economic Work Conference in mid-December, while China’s GDP growth targets are expected to be set out in the National People’s Congress in March next year. Fig. 2. Effective policy implementation can only begin after the specific roles of the different Politburo members have been decided. Therefore, the Central Economic Work Conference in December and the upcoming sessions in March are key events that will have a significant impact on the direction of China’s economy going forward.

Fig. 2 Key political and policy events in China

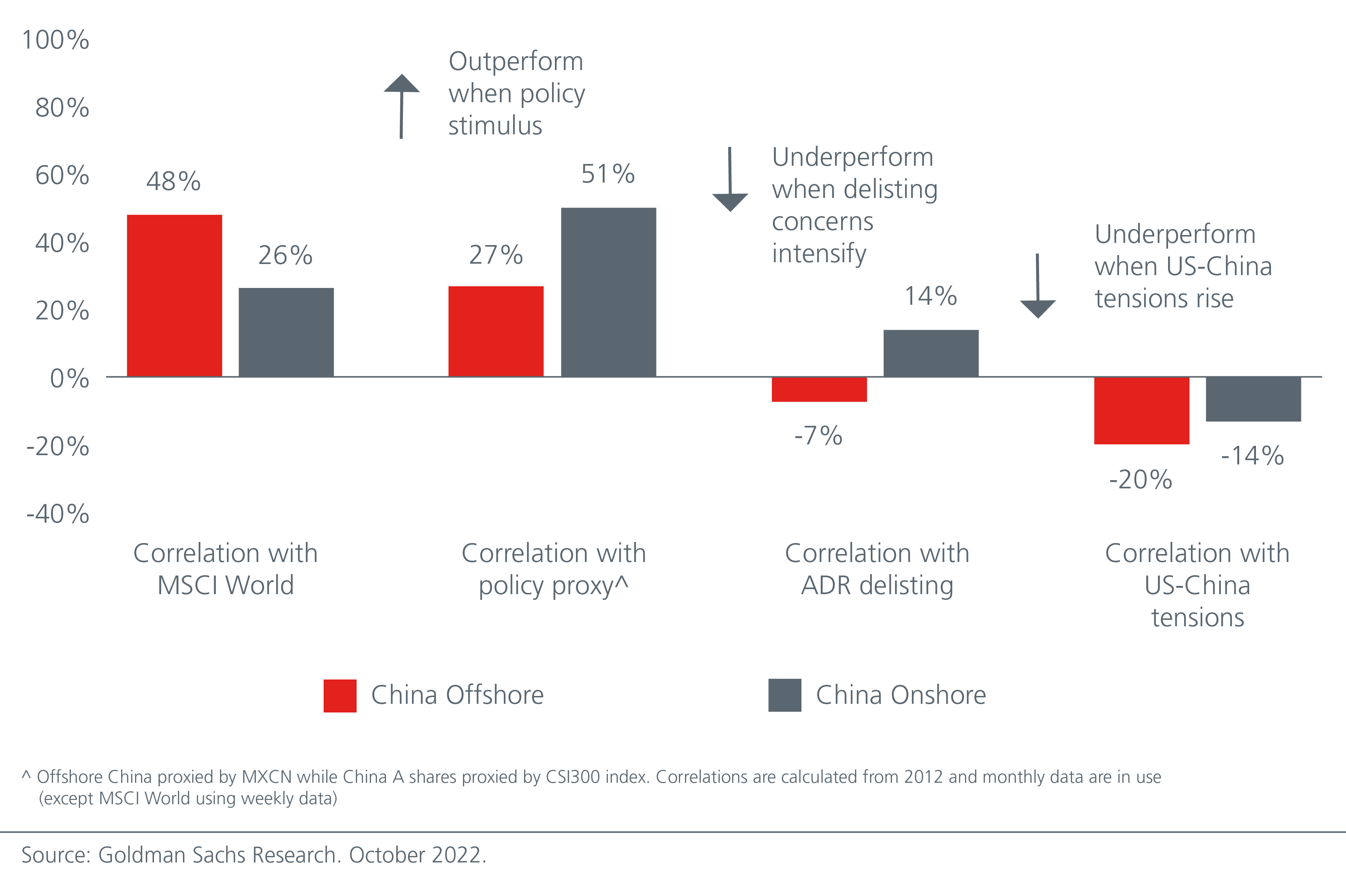

Compared to the China off-shore market, China A-shares equities are more correlated to domestic macro factors and liquidity conditions, and are less correlated to MSCI World, potentially offering greater diversification to global portfolios. Fig. 3.

Fig. 3. China A-shares more correlated to domestic factors

In terms of sector positioning within the China A-share market, we will be focusing on the structural opportunities aligned with the key words “development” and “safety” which were outlined in the Report. As shown in Fig. 1., the mention of “safety” was significantly higher compared to 5 years ago. We believe that there will be increasing policy support towards self-sufficiency, energy safety and technology independency. As such, we continue to look for new opportunities in the new energy, automation, information security, electrical/medical equipment sectors, favouring companies that have core technology competencies and a globally competitive edge.

We expect China’s Dynamic Zero-COVID policy to remain in place until at least the 2nd quarter of 2023. The policy was considered a success in China, as highlighted in the Report, and there are no imminent signs of a relaxation. We anticipate that ultimately, the Chinese equity markets will trade higher leading up to any changes to the policy. This will be in line with the performances of other markets which we have observed, ahead of their respective economic re-openings.

Interesting reads

Singapore by Eastspring Investments (Singapore) Limited (UEN: 199407631H)

Australia (for wholesale clients only) by Eastspring Investments (Singapore) Limited (UEN: 199407631H), which is incorporated in Singapore, is exempt from the requirement to hold an Australian financial services licence and is licensed and regulated by the Monetary Authority of Singapore under Singapore laws which differ from Australian laws

Hong Kong by Eastspring Investments (Hong Kong) Limited and has not been reviewed by the Securities and Futures Commission of Hong Kong.

Indonesia by PT Eastspring Investments Indonesia, an investment manager that is licensed, registered and supervised by the Indonesia Financial Services Authority (OJK).

Malaysia by Eastspring Investments Berhad (200001028634/ 531241-U) and Eastspring Al-Wara’ Investments Berhad (200901017585 / 860682-K) and has not been reviewed by Securities Commission of Malaysia.

Thailand by Eastspring Asset Management (Thailand) Co., Ltd.

United States of America (for institutional clients only) by Eastspring Investments (Singapore) Limited (UEN: 199407631H), which is incorporated in Singapore and is registered with the U.S Securities and Exchange Commission as a registered investment adviser.

European Economic Area (for professional clients only) and Switzerland (for qualified investors only) by Eastspring Investments (Luxembourg) S.A., 26, Boulevard Royal, 2449 Luxembourg, Grand-Duchy of Luxembourg, registered with the Registre de Commerce et des Sociétés (Luxembourg), Register No B 173737.

Chile (for institutional clients only) by Eastspring Investments (Singapore) Limited (UEN: 199407631H), which is incorporated in Singapore and is licensed and regulated by the Monetary Authority of Singapore under Singapore laws which differ from Chilean laws.

The afore-mentioned entities are hereinafter collectively referred to as Eastspring Investments.

The views and opinions contained herein are those of the author, and may not necessarily represent views expressed or reflected in other Eastspring Investments’ communications. This document is solely for information purposes and does not have any regard to the specific investment objective, financial situation and/or particular needs of any specific persons who may receive this document. This document is not intended as an offer, a solicitation of offer or a recommendation, to deal in shares of securities or any financial instruments. It may not be published, circulated, reproduced or distributed without the prior written consent of Eastspring Investments. Reliance upon information in this document is at the sole discretion of the reader. Please carefully study the related information and/or consult your own professional adviser before investing.

Investment involves risks. Past performance of and the predictions, projections, or forecasts on the economy, securities markets or the economic trends of the markets are not necessarily indicative of the future or likely performance of Eastspring Investments or any of the funds managed by Eastspring Investments.

Information herein is believed to be reliable at time of publication. Data from third party sources may have been used in the preparation of this material and Eastspring Investments has not independently verified, validated or audited such data. Where lawfully permitted, Eastspring Investments does not warrant its completeness or accuracy and is not responsible for error of facts or opinion nor shall be liable for damages arising out of any person’s reliance upon this information. Any opinion or estimate contained in this document may subject to change without notice.

Eastspring Investments companies (excluding joint venture companies) are ultimately wholly owned/indirect subsidiaries of Prudential plc of the United Kingdom. Eastspring Investments companies (including joint venture companies) and Prudential plc are not affiliated in any manner with Prudential Financial, Inc., a company whose principal place of business is in the United States of America or with the Prudential Assurance Company Limited, a subsidiary of M&G plc (a company incorporated in the United Kingdom).