Executive Summary

- Tariffs will increase inflation, reduce consumption and hurt business investment spending in the US. Slower economic and earnings growth no longer justify US equities’ premium valuations. We expect the S&P 500 to derate.

- Emerging Markets’ cheap valuations and increasingly favourable growth differential versus the Developed Markets position it well to capture some of the diversification flows from US equities.

- We are no strangers to volatility and remain focused on identifying names at depressed valuations. We are looking at markets where company specific factors are pushing up return on equity as well as selected bright spots within Latin America.

US tariff changes continue to create uncertainty. The 90-day pause on tariffs, except for China, and the announced exemptions illustrate the unpredictability of US trade policy. What might unfold between now and the end of the 90-day pause in July remains unclear.

That aside, the current effective US tariff rate is still close to 20%, up from 2.4% last year. This will increase inflation, reduce consumption by reducing real incomes, and damage business investment spending in the US. As such, US growth is expected to come in at sub-1% this year with a negative effect on corporate earnings. This slower growth is likely to persist into 2026.

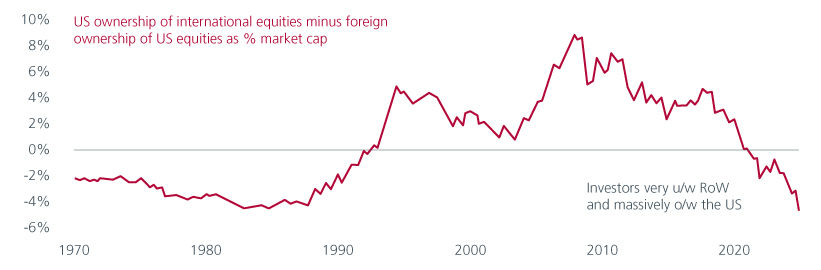

With US equities still priced at a premium at a 12-month forward price to earnings ratio of around 20x, sub trend US growth for the next 12 to 18 months suggests that US equities should de-rate to at least its 35-year historical trading average of 18x. Given the significant weightings in US equities among global portfolios (See Fig. 1), investors are likely to seek greater diversification.

Fig. 1. Investors are massively OW US equities

Source: Federal Reserve. HSBC. April 2025.

EM is well positioned

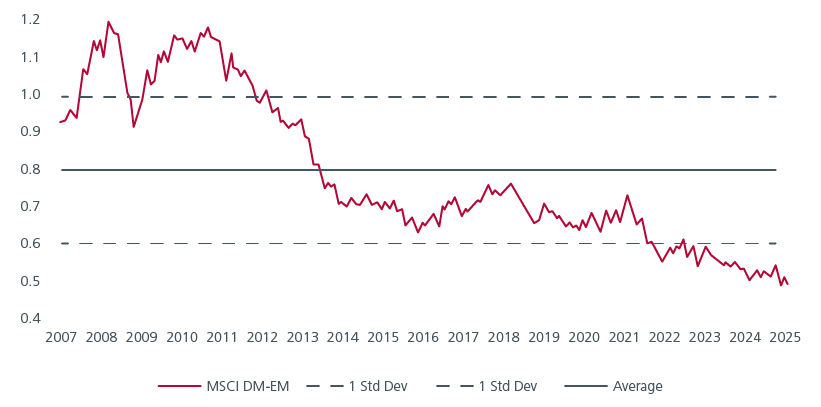

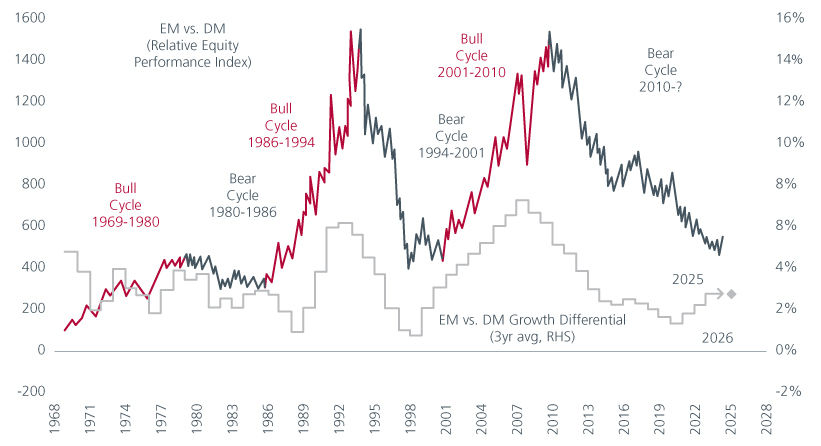

We believe that Emerging Markets (EMs) are well-positioned to attract some of these flows. For one, valuations are very cheap relative to the developed markets (DMs) (Fig. 2). We could also be at an inflection point where the growth differential between EMs and DMs stabilizes and potentially widens. Historically, EMs have outperformed DMs when this growth differential rises. See Fig. 3.

Fig. 2. MSCI EM relative to MSCI World trailing PB(x)

Source: MSCI. Refinitiv Datastream. Eastspring Investments. As of March 2025. Notes: PB = price to book. DM is MSCI World Index. EM is MSCI Emerging Market Index.

Fig. 3. EM vs DM: Relative performance vs growth differential

Source: FactSet, Goldman Sachs Global Investment Research. 7 April 2025. EM: MSCI Emerging Markets Index. DM: MSCI World Index. Relative Equity Performance Index rebased to 100 at 1968.

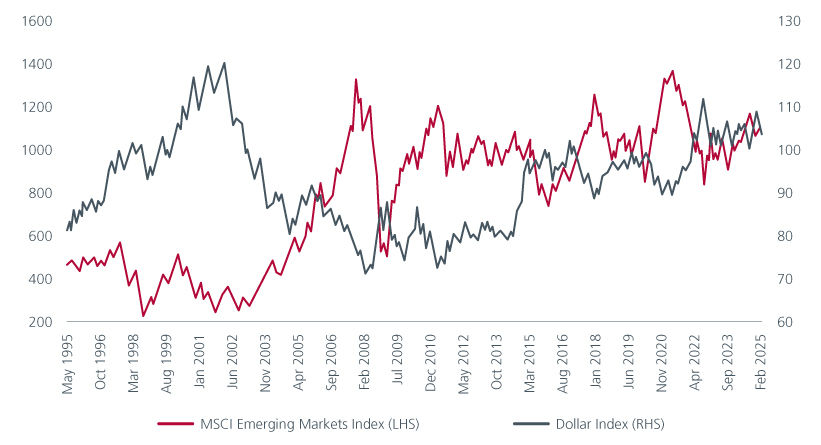

Amid the recent heightened market volatility, it is interesting to note that the US dollar has declined 8.3% year to date, while other typical safe havens like gold and the Swiss franc have appreciated 26.0% and 10.0% respectively. With the Federal Reserve more likely to cut than to lift interest rates as US growth slows further, and given President Trump’s desire for a weaker dollar, a peak in the USD would be positive for EM assets, as long as investor risk appetite holds. Historically, EMs and the USD have shared an inverse relationship. Fig. 4.

Fig. 4. Emerging markets go up when the USD goes down

Source: Bloomberg. April 2025.

A weaker USD could boost higher carry EM currencies. It could also provide more room for rate cuts given EM central banks’ concerns about exchange rate stability and passthrough to inflation. We note that policy is already rapidly easing in Asia following recent moves by policymakers in India, Korea and Singapore. We expect the Bank of Korea and Bank of Thailand to cut rates again in the coming months. We see plenty of scope for easing in non-Asia EM too. A weaker USD could provide a positive feedback loop between lower rates, higher economic growth and capital inflows for EMs.

Emerging Markets in a post tariff world

While few countries have been spared from the US’ tariffs, there are relative winners within EMs. Countries that can deliver policy stimulus can offset some of the tariff shock. In earlier commentaries, we had highlighted the potential for India and China to navigate the tariffs. We focus on Latin America (LatAm) and Central & Eastern Europe, Middle East and Africa (CEEMEA) in this article.

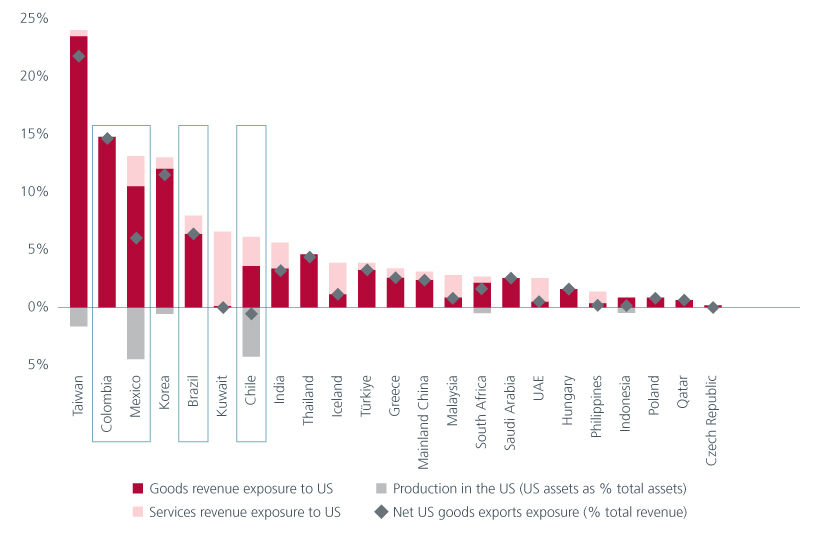

Prior to the 2nd April tariff announcements, LatAm currencies had depreciated more than those of EMEA and Asia. On a year on year basis, LatAm currencies have depreciated 15% against the USD, while EMEA and Asia FX have fallen 4% and 2.5%1. This was partly due to market expectations that the LatAm countries were going to be among the hardest hit by the tariffs within EMs. LatAm’s high goods revenue exposure to the US also exacerbated market concerns. Fig. 5.

Fig. 5. EM countries' revenue exposure to US

Source: FTSE Russell, Factset, HSBC. 20 February 2025.

However, the tariff announcements to date suggest that LatAm is a relative winner in the EMs. For one, the absence of incremental tariffs (at the point of writing) on Mexico was a positive surprise. For now, there are no tariffs on USMCA compliant goods; and while the US has slapped a 25% tariff on non-compliant goods; future exemptions could lower the effective tariff rate to 12%. Given the higher tariffs imposed on other manufacturing locations, the near shoring theme appears intact and should be positive for Mexico.

Brazil should also be less impacted by tariffs given its relatively closed economy – 80 to 85% of GDP is domestically driven. Historically, Brazilian equities have benefited from a weaker USD and lower rates. With the Brazilian and Mexico equity markets trading well below their historic averages, at 7.7x and 11.4x 2025 price to earnings respectively, we are finding fertile ground to find names at depressed valuations. In particular, we like rate sensitive names in Brazil.

The CEEMEA region is also relatively less affected with a GDP-weighted average tariff of 11.4% although there is variability within the region. Reciprocal tariff rates for the larger markets in the Middle East like Qatar, Saudi Arabia and UAE are at the lower end at 10% although the region is expected to be hurt by lower oil prices. For Turkey, the outlook for Europe matters more as it exports more to the European Union (8.2% of GDP) than the US (1.2% of GDP). At the same time, Turkey could benefit from reshoring of manufacturing from China.

The CE3 economies (Poland, Czech Republic, and Hungary) face 20% tariffs that are consistent with the EU's rates. Both Poland and the Czech Republic have less than 1% of their revenues tied to the US, while Hungary, with approximately 1.6% of its revenues dependent on the US, is the most vulnerable due to its substantial auto manufacturing industry. Meanwhile, South Africa’s 30% tariff rates could end up lower following exemptions.

No stranger to volatility

EMs’ attractive valuations and increasing favourable growth differential versus the DMs position it well to benefit from a weaker USD and potential diversification flows away from US equities. While few countries have been spared from the US’ reciprocal tariffs, there is significant variability within EMs in terms of exposure to US revenues, potential market share gains/losses and central bank responses. This backdrop presents significant opportunities for active managers to add value. EM investors are no strangers to market volatility. We are accustomed to navigating the complexities and fluctuations inherent in these markets. As such, amid the market volatility, we continue to focus on delivering long-term alpha by staying disciplined and uncovering high names at depressed valuations.

Interesting reads

Sources:

1 As of 6 March 2025.

Singapore by Eastspring Investments (Singapore) Limited (UEN: 199407631H)

Australia (for wholesale clients only) by Eastspring Investments (Singapore) Limited (UEN: 199407631H), which is incorporated in Singapore, is exempt from the requirement to hold an Australian financial services licence and is licensed and regulated by the Monetary Authority of Singapore under Singapore laws which differ from Australian laws

Hong Kong by Eastspring Investments (Hong Kong) Limited and has not been reviewed by the Securities and Futures Commission of Hong Kong.

Indonesia by PT Eastspring Investments Indonesia, an investment manager that is licensed, registered and supervised by the Indonesia Financial Services Authority (OJK).

Malaysia by Eastspring Investments Berhad (200001028634/ 531241-U) and Eastspring Al-Wara’ Investments Berhad (200901017585 / 860682-K).

Thailand by Eastspring Asset Management (Thailand) Co., Ltd.

United States of America (for institutional clients only) by Eastspring Investments (Singapore) Limited (UEN: 199407631H), which is incorporated in Singapore and is registered with the U.S Securities and Exchange Commission as a registered investment adviser.

European Economic Area (for professional clients only) and Switzerland (for qualified investors only) by Eastspring Investments (Luxembourg) S.A., 26, Boulevard Royal, 2449 Luxembourg, Grand-Duchy of Luxembourg, registered with the Registre de Commerce et des Sociétés (Luxembourg), Register No B 173737.

Chile (for institutional clients only) by Eastspring Investments (Singapore) Limited (UEN: 199407631H), which is incorporated in Singapore and is licensed and regulated by the Monetary Authority of Singapore under Singapore laws which differ from Chilean laws.

The afore-mentioned entities are hereinafter collectively referred to as Eastspring Investments.

The views and opinions contained herein are those of the author, and may not necessarily represent views expressed or reflected in other Eastspring Investments’ communications. This document is solely for information purposes and does not have any regard to the specific investment objective, financial situation and/or particular needs of any specific persons who may receive this document. This document is not intended as an offer, a solicitation of offer or a recommendation, to deal in shares of securities or any financial instruments. It may not be published, circulated, reproduced or distributed without the prior written consent of Eastspring Investments. Reliance upon information in this document is at the sole discretion of the reader. Please carefully study the related information and/or consult your own professional adviser before investing.

Investment involves risks. Past performance of and the predictions, projections, or forecasts on the economy, securities markets or the economic trends of the markets are not necessarily indicative of the future or likely performance of Eastspring Investments or any of the funds managed by Eastspring Investments.

Information herein is believed to be reliable at time of publication. Data from third party sources may have been used in the preparation of this material and Eastspring Investments has not independently verified, validated or audited such data. Where lawfully permitted, Eastspring Investments does not warrant its completeness or accuracy and is not responsible for error of facts or opinion nor shall be liable for damages arising out of any person’s reliance upon this information. Any opinion or estimate contained in this document may subject to change without notice.

Eastspring Investments companies (excluding joint venture companies) are ultimately wholly owned/indirect subsidiaries of Prudential plc of the United Kingdom. Eastspring Investments companies (including joint venture companies) and Prudential plc are not affiliated in any manner with Prudential Financial, Inc., a company whose principal place of business is in the United States of America or with the Prudential Assurance Company Limited, a subsidiary of M&G plc (a company incorporated in the United Kingdom).