Summary

We provide key takeaways from Eastspring’s Asian Expert webinar “Is it time to relook at bonds?”, where Mark Redfearn from PPM America and Clement Chong from Eastspring Investments shared their insights on the US and Asian bond markets.

1. Valuations are attractive

It was not that long ago that the market value of negative yielding debt soared above USD18 trillion1, as global central banks cut interest rates and bought large amounts of bonds in the wake of the COVID-19 pandemic. The amount of negative yielding debt has since dwindled to zero as interest rates rose globally.

Bond yields now in many countries are at multi-year highs, offering investors a once in a decade opportunity to enjoy attractive levels of income and potential capital gains when yields head lower in the coming months and years.

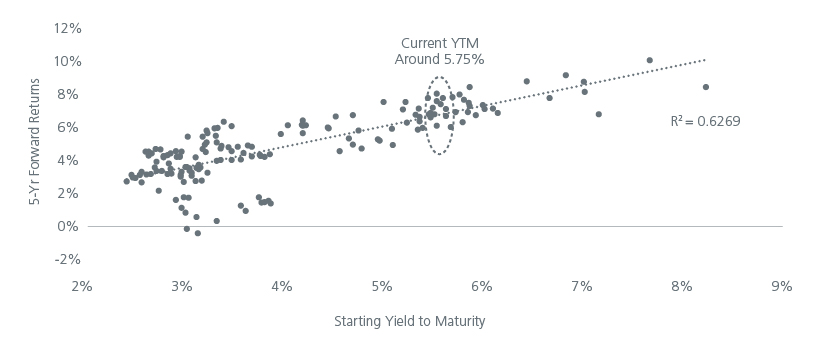

Fig. 1. shows that over the last 13 years, buying US bonds at current levels of around 5.75% has delivered 5-year forward returns of 6% p.a. The figure also shows that historically, there has been very few instances where yields have moved higher from here, suggesting that current yields provide investors with very attractive entry levels.

Fig. 1. Starting yields and forward returns are closely correlated

Source: FactSet, Morningstar. Monthly yields for the Bloomberg US Credit Index from January 2005 through July 2018 and 5-year forward returns from the Jan-05 to Dec-09 period through the Aug-18 to Jul-23 period.

2. Cash rates will fall (eventually)

Cash rates are unlikely to stay high indefinitely. At the Federal Open Market Committee meeting in September, the Federal Reserve (Fed) indicated that it would start cutting interest rates from 2024. In the coming months, as both the US economy and inflation slows further, it would not be surprising for bond markets to move ahead of the Fed and for bond yields to start declining even before the Fed’s first rate cut. As such, investors may want to look beyond the current cash rate levels and instead focus on the upside potential of bonds.

The recent spike in oil prices has raised concerns over the outlook for inflation, and the prospects for rate cuts. Slowing global growth plus the approaching end of the driving season in the US should help to dampen oil demand. In addition, Saudi Arabia is unlikely to extend its production cuts indefinitely and risk losing further market share. All these factors should help to keep a lid on oil prices.

Asia’s inflation has been relatively more contained than the US’, as the region has not experienced the same extent of demand-supply imbalances, especially in the labour market. That said, the recent rise in oil and food prices bears monitoring although historically, Asian central banks have shown the willingness to cushion the impact of high oil prices via subsidies.

The resilience of the US economy to date has given the Fed confidence to keep rates high for longer. However, the full impact of high interest rates has yet to fully filter through the US economy, particularly in home mortgages where many households enjoy 30-year fixed rate terms, as well as in the commercial real estate and corporate debt segments. A faster than expected deterioration of the US economy could prompt the Fed to pivot earlier. Asian central banks are more likely to follow the Fed’s lead.

3. Bonds are diversifiers again

Given current yields, bonds can regain their roles as diversifiers in portfolios again as the income they generate should help buffer portfolios against potential equity market volatility. With the ongoing uncertainty over economic growth, it may be prudent for investors to refocus on income and principal preservation in their portfolios. While equities participate on the upside in earnings expansion, bonds are a low beta strategy. At current yields, bonds potentially offer equity-like returns but with lower volatility.

As mentioned earlier, the impact of higher interest rates is still making its way through the US economy and is likely to affect corporate margins and earnings eventually. Over in Asia, China is still growing but at a much lower rate than what investors are used to or anticipated. Slow growth in China and the developed economies has weighed on the outlooks of the export-dependent economies in Asia, although countries with large domestic populations such as India, Indonesia and the Philippines have been more resilient.

Investors should nevertheless retain a thoughtful approach towards their bond allocations as the recent sharp selloffs in the bond markets in October 2022 and March 20232 show that market depth and liquidity are lower than perceived.

Where are the opportunities?

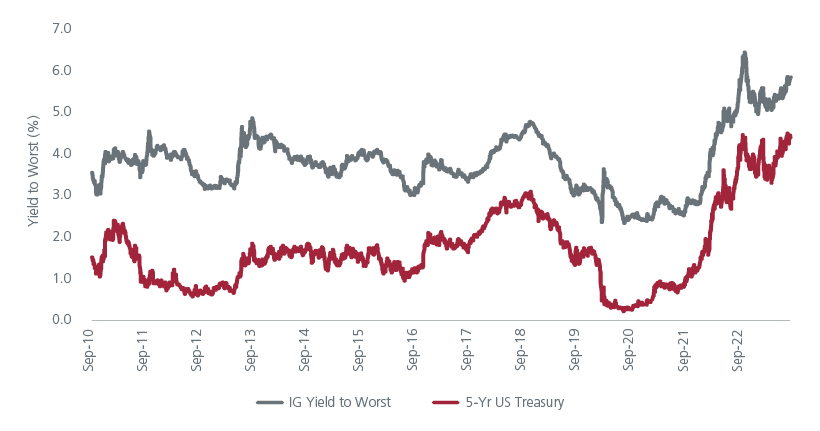

In both the US and Asia, Investment Grade credits are expected to better weather the higher costs of funding given their stronger credit profiles. The duration of US Investment Grade is roughly twice that of its High Yield counterpart3. This suggests that US Investment Grade bonds on average are likely to enjoy greater capital appreciation than US high yield bonds when bond yields fall in the coming years. Over in Asia, the yield to worst for Investment Grade credits is at its highest since 2008. See Fig. 2. This presents the potential for capital appreciation when the Fed starts to pivot.

Fig. 2. Asian Investment Grade credit market is in a sweet spot

Source: JP Morgan, Bloomberg, September 2023. JACI Investment Grade Index.

Within US Investment Grade credits, single A-rated bonds are favoured over BBB-rated bonds. In addition, there is a preference for highly regulated sectors such as utilities, energy and large national champion banks which tend to be better capitalised. Meanwhile, the USD is expected to remain supported by interest rate differentials.

In Asia, there is a preference for local government bonds especially from countries that have stronger fiscal and current account positions, better inflation dynamics and the flexibility to cut rates at some point. Since Asian currencies may be weighed down in the near term by a weak RMB, it may be appropriate to assess valuations on a currency hedged basis. The valuations of Singapore dollar (SGD) corporate bonds and Malaysian government bonds look compelling on a currency hedged basis. Besides attractive yields, SGD corporate bonds also offer greater stability.

PPM America is a US-based asset manager and is the investment sub-manager for Eastspring’s US bond strategies. Please click on this link to watch a replay of the webinar.

Interesting reads

Sources:

1 Bloomberg. 2020

2 US regional banking crisis.

3 The indices used for this measurement are the Bloomberg US Corporate Index and the ICE BofA US High Yield Index, which have effective durations of 6.92 and 3.60 respectively as of 31 August.

This document is produced by Eastspring Investments (Singapore) Limited and issued in:

Singapore by Eastspring Investments (Singapore) Limited (UEN: 199407631H)

Australia (for wholesale clients only) by Eastspring Investments (Singapore) Limited (UEN: 199407631H), which is incorporated in Singapore, is exempt from the requirement to hold an Australian financial services licence and is licensed and regulated by the Monetary Authority of Singapore under Singapore laws which differ from Australian laws

Hong Kong by Eastspring Investments (Hong Kong) Limited and has not been reviewed by the Securities and Futures Commission of Hong Kong.

Indonesia by PT Eastspring Investments Indonesia, an investment manager that is licensed, registered and supervised by the Indonesia Financial Services Authority (OJK).

Malaysia by Eastspring Investments Berhad (200001028634/ 531241-U) and Eastspring Al-Wara’ Investments Berhad (200901017585 / 860682-K) and has not been reviewed by Securities Commission of Malaysia.

Thailand by Eastspring Asset Management (Thailand) Co., Ltd.

United States of America (for institutional clients only) by Eastspring Investments (Singapore) Limited (UEN: 199407631H), which is incorporated in Singapore and is registered with the U.S Securities and Exchange Commission as a registered investment adviser.

European Economic Area (for professional clients only) and Switzerland (for qualified investors only) by Eastspring Investments (Luxembourg) S.A., 26, Boulevard Royal, 2449 Luxembourg, Grand-Duchy of Luxembourg, registered with the Registre de Commerce et des Sociétés (Luxembourg), Register No B 173737.

Chile (for institutional clients only) by Eastspring Investments (Singapore) Limited (UEN: 199407631H), which is incorporated in Singapore and is licensed and regulated by the Monetary Authority of Singapore under Singapore laws which differ from Chilean laws.

The afore-mentioned entities are hereinafter collectively referred to as Eastspring Investments.

The views and opinions contained herein are those of the author, and may not necessarily represent views expressed or reflected in other Eastspring Investments’ communications. This document is solely for information purposes and does not have any regard to the specific investment objective, financial situation and/or particular needs of any specific persons who may receive this document. This document is not intended as an offer, a solicitation of offer or a recommendation, to deal in shares of securities or any financial instruments. It may not be published, circulated, reproduced or distributed without the prior written consent of Eastspring Investments. Reliance upon information in this document is at the sole discretion of the reader. Please carefully study the related information and/or consult your own professional adviser before investing.

Investment involves risks. Past performance of and the predictions, projections, or forecasts on the economy, securities markets or the economic trends of the markets are not necessarily indicative of the future or likely performance of Eastspring Investments or any of the funds managed by Eastspring Investments.

Information herein is believed to be reliable at time of publication. Data from third party sources may have been used in the preparation of this material and Eastspring Investments has not independently verified, validated or audited such data. Where lawfully permitted, Eastspring Investments does not warrant its completeness or accuracy and is not responsible for error of facts or opinion nor shall be liable for damages arising out of any person’s reliance upon this information. Any opinion or estimate contained in this document may subject to change without notice.

Eastspring Investments companies (excluding joint venture companies) are ultimately wholly owned/indirect subsidiaries of Prudential plc of the United Kingdom. Eastspring Investments companies (including joint venture companies) and Prudential plc are not affiliated in any manner with Prudential Financial, Inc., a company whose principal place of business is in the United States of America or with the Prudential Assurance Company Limited, a subsidiary of M&G plc (a company incorporated in the United Kingdom).