Eastspring Investments

Feb 2023 | 6 min read

Asia's natural resources are among the richest and most diverse in the planet1 , many of which have underpinned the region’s rapid growth for decades. Asian countries are some of the world’s top producers of agricultural, fishing, forest, and mining products. But this growth has come at a price to the environment. With climate change being the single biggest threat to the region’s future growth, Asian governments are increasingly incorporating sustainability in their economic agendas.

Given that Asia’s energy and transport sectors are responsible for a large portion of the region’s carbon emissions, many of the sustainability projects are centred on clean energy transition and green transport. We believe that the opportunities for sustainable growth are enormous as the region accelerates its decarbonisation efforts.

In Case for Asia article, we highlighted sustainability as one of the key future growth drivers for the region. Sustainability starts with the “greening” of resources. The biggest impact will be on the region’s resources industry as it is typically at the start of any global value chain. To this end, the region is powering ahead with developing clean energy resources, namely renewable energy, and hydrogen.

Renewable energy on the rise

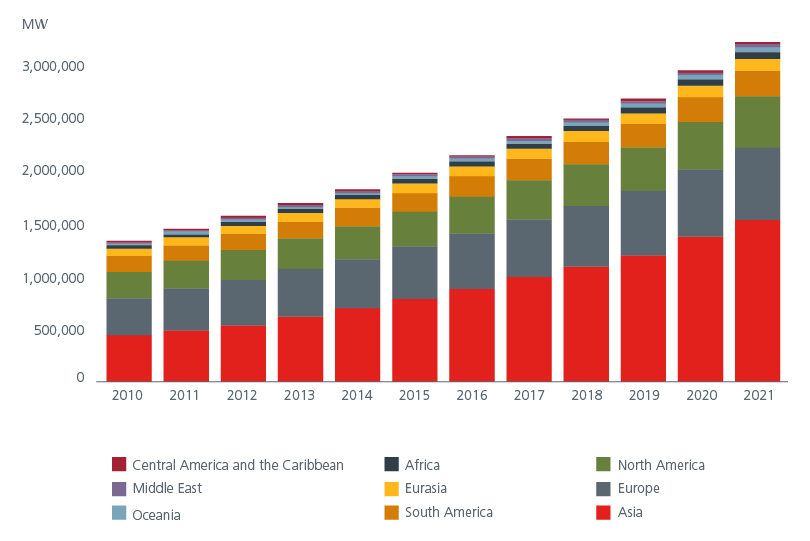

Renewable energy (RE) is a form of clean energy derived from nature i.e., solar energy, wind energy, hydroelectric energy, geothermal energy, and biomass. Asia has approximately 45% of the global share of installed RE capacity with China, India, and Australia owning half of it. See Fig 1. Within ASEAN, more than 80% share of RE capacity sits in Vietnam, Thailand, the Philippines, Malaysia, and Indonesia.2

Fig 1: Renewable capacity by regions

Source: IRENA, July 2022

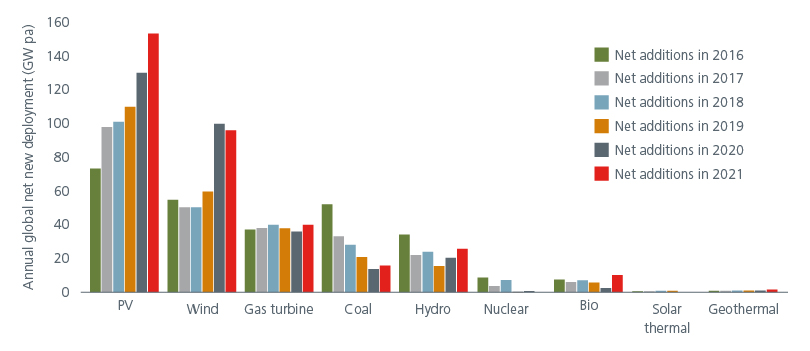

Three quarters of global net generation capacity additions in recent years have been in solar and wind generators.3 See Fig 2. Most countries are self-sufficient when it comes to solar and/or wind resources; many Asian countries can harness all-year round of solar irradiation at a low cost to the environment. A key advantage of renewables is there is no risk of supply disruption in case of a war or trade dispute.

Fig 2: Global net generation capacity additions 2016-2021

Source: IRENA, CER, GWEC, WNA, GEM, ITRPV, IEA 2021

Asia’s overall power mix is forecast to see a continuous increase in renewable capacity to 63% by 2035, from 40% in 2022. Various countries have ambitious renewable energy roadmaps. For example, Malaysia has a national renewable energy target of 31% by 2025, backed by large hydro and solar technology. China's 14th Five-Year Plan states a target of requiring 33% of electricity consumption to come from renewables by 2025. Meanwhile India aims to get 50% of its electricity requirements from renewable energy sources by 2030.

Given these targets, the investment opportunities are wide, ranging from RE power producers to solar and wind turbine and battery manufacturers to companies extracting minerals such as nickel and lithium which are used for batteries and solar panels.

Hydrogen can be a game changer

Hydrogen is another energy resource that is generating significant interest in the region. It can be produced by natural gas, coal, biomass, and even renewable power like solar and wind. One of the key benefits of hydrogen is its potential for long-duration energy storage. As such it can be utilised as and when needed. Hydrogen can also be liquefied and transported easily. Plus, being light weight, it is a good alternative to jet fuel.

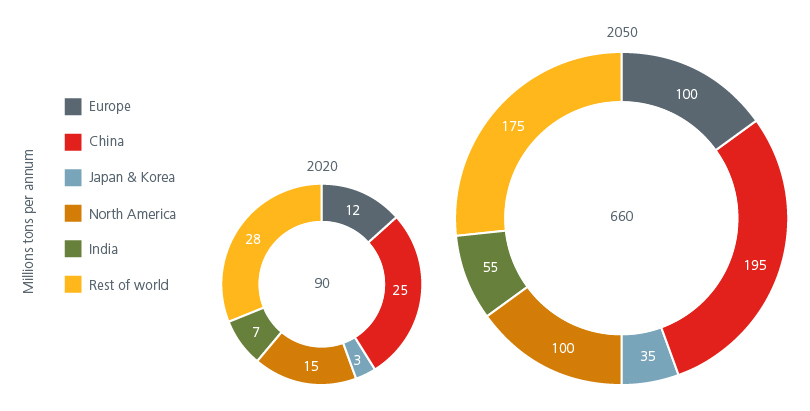

Hydrogen is starting to feature prominently in many countries’ long-term energy strategies. Some Asian countries such as Japan, Korea and India even have national hydrogen strategies; Japan was one of the earliest to adopt the ‘Basic Hydrogen Strategy’ in 2017. By 2050, hydrogen will be a major part of energy markets across the globe. See Fig 3. China, India, Japan, South Korea, Europe, and North America will account for 75% of global hydrogen demand.4

Fig 3: Hydrogen demand by region

Source: Hydrogen Council and McKinsey & Company, October 2022

Currently most of the hydrogen is produced from fossil fuels such as coal and natural gas and termed “grey” as carbon is still emitted during the process. To meet net zero emission targets, countries are shifting their focus to “green” hydrogen – the cleanest form of hydrogen. Green hydrogen is achieved via a process of electrolysis powered by renewable energy sources.

Asia is fast becoming a production base for green hydrogen. China is building the world’s largest solar-powered green hydrogen factory in Xinjiang.5 Likewise India is banking on its inexpensive solar power to position the country as a cost leader in green hydrogen while Korea targets to increase the clean hydrogen ratio to 50% in 30 years and 100% in 50 years.

As the energy transition to hydrogen gains pace, investment opportunities will also emerge along the entire value chain. Manufacturers of electrolysers needed to produce green hydrogen will be in demand as will companies that provide storage facilities and develop pipelines to transport hydrogen.

Raw materials bolster green technologies

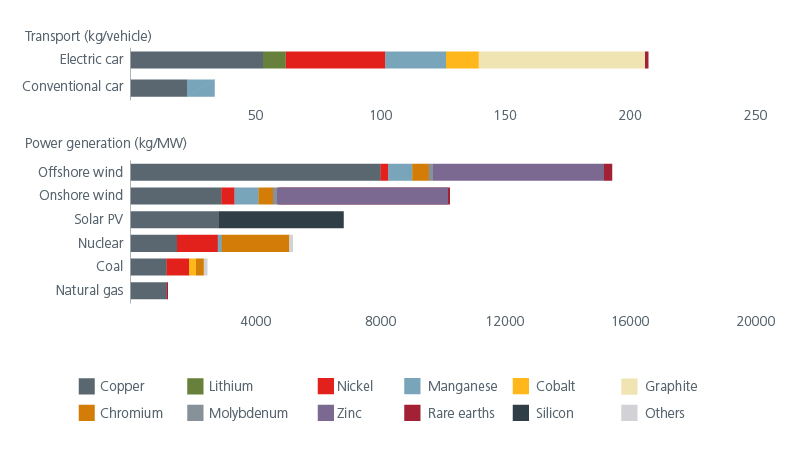

The demand for raw materials is set to rise with the transition to clean energy; copper, zinc, silicon, nickel are some of the key minerals used in clean energy technologies. Lithium, nickel, cobalt, manganese, and graphite are important for battery performance. Rare earth elements are needed for permanent magnets that go into wind turbines. Copper and aluminium are vital for electricity networks.

Fortunately, Asia is rich in many of these materials. For example, Indonesia and Philippines have large reserves of nickel while China has copper, graphite, lithium, and rare earth. Others such as bauxite, tin and rare earth elements can also be found throughout the region. Investing in the region’s mining companies can be one way to capitalise this opportunity.

Fig 4: Minerals used in selected clean energy technologies

Source: IEA March 2022

Given the transportation industry is one of the largest carbon emitters in the region, the switch to electric vehicles (EVs) plays a big role in Asia’s net zero journey. By 2025, 20% of all vehicles in the region will be electric.6 Currently China is the world’s largest EV manufacturer. Meanwhile Thailand, Indonesia and Vietnam are also pushing ahead to develop their domestic EV markets. The EV investment opportunity extends beyond manufacturers to battery makers, a key component of EVs. As the demand for EVs and batteries rise, so too will the demand for critical minerals required to produce them.

Growing demand for alternative foods

Besides the opportunities to be had from Asia’s clean energy transition, there are other upcoming sectors that deserve special mention, namely food. By 2030, almost half of the global population will live in Asia. As such, ensuring the region’s food security is vital. Food resilience is now part of many national agendas with the aim of achieving self-sufficiency. Moreover, as Asia’s agriculture sector contributes significantly to climate change, improving farming practices and pushing ahead with innovative food alternatives will help support the region’s sustainability agenda.

There is growing interest in tech-based food solutions, especially alternative protein products. Demand for plant-based meat sector is on the rise; according to Bloomberg Intelligence, Asia Pacific will likely dominate the global plant-based protein market, reaching USD64.8 billion by 2030 from USD13.5 billion in 2020.7 The good news is that many Asian countries are able to also supply the raw materials (mung beans, soybeans etc.) required to manufacture plant-based protein products.

Agrifood waste is another area to note given that it is a potential resource to produce biofuels and value-added chemicals; Indonesia’s liquid waste from palm oil production can be converted into biogas while fibres from banana waste are being used to create fashion products. Agri companies that adopt green tech-based solutions to have better harvests and mitigate food waste will likely do well.

Key to sustainability is circularity

To truly achieve sustainable development across the region, it is also vital to promote a circular economy. A circular economy aims to reduce, reuse, and recycle materials. By reusing materials, the circular economy can turn waste into a resource and unlock many new business opportunities and create a host of new jobs, from recycling and repair to digital and innovation-driven work.

Several Asian countries have adopted ad hoc circular economy policies. But to achieve a regional circular economy, a formal framework is needed. The good news is that ASEAN adopted a Framework for Circular Economy in October 2021 in which five strategic priorities were identified; one amongst them is the efficient use of energy and other resources. Nonetheless, more integrated and holistic policies are needed to bring about tangible economic and environmental benefits.

Contributors:

Yuni Husain, Equity Analyst, Eastspring Indonesia

Paul Kim, Head of Equities, Eastspring Korea

Lilian See, Head of Equity Research & Lim Wei Ren, Sustainability Manager, Eastspring Malaysia

This is the last in our series of 4 articles where we provide insights into Asia and the region’s consumer, supply chains and resources.

Sources:

1 https://www.adb.org/features/natural-resources-conservation-asia-adbs-take

2 https://www.mckinsey.com/featured-insights/future-of-asia/green-growth-capturing-asias-5-trillion-green-business-opportunity

3 https://hk.boell.org/en/2022/10/31/solar-wind-and-clean-hydrogen-asias-energy-transition-without-hype

4 https://hydrogencouncil.com/wp-content/uploads/2022/10/Global-Hydrogen-Flows.pdf

5 https://www.scmp.com/news/china/science/article/3188751/china-building-worlds-largest-green-hydrogen-factory

6 International Renewable Energy Agency

7 https://www.bloomberg.com/company/press/plant-based-foods-market-to-hit-162-billion-in-next-decade-projects-bloomberg-intelligence/

Singapore by Eastspring Investments (Singapore) Limited (UEN: 199407631H)

Australia (for wholesale clients only) by Eastspring Investments (Singapore) Limited (UEN: 199407631H), which is incorporated in Singapore, is exempt from the requirement to hold an Australian financial services licence and is licensed and regulated by the Monetary Authority of Singapore under Singapore laws which differ from Australian laws

Hong Kong by Eastspring Investments (Hong Kong) Limited and has not been reviewed by the Securities and Futures Commission of Hong Kong.

Indonesia by PT Eastspring Investments Indonesia, an investment manager that is licensed, registered and supervised by the Indonesia Financial Services Authority (OJK).

Malaysia by Eastspring Investments Berhad (200001028634/ 531241-U) and Eastspring Al-Wara’ Investments Berhad (200901017585 / 860682-K).

Thailand by Eastspring Asset Management (Thailand) Co., Ltd.

United States of America (for institutional clients only) by Eastspring Investments (Singapore) Limited (UEN: 199407631H), which is incorporated in Singapore and is registered with the U.S Securities and Exchange Commission as a registered investment adviser.

European Economic Area (for professional clients only) and Switzerland (for qualified investors only) by Eastspring Investments (Luxembourg) S.A., 26, Boulevard Royal, 2449 Luxembourg, Grand-Duchy of Luxembourg, registered with the Registre de Commerce et des Sociétés (Luxembourg), Register No B 173737.

Chile (for institutional clients only) by Eastspring Investments (Singapore) Limited (UEN: 199407631H), which is incorporated in Singapore and is licensed and regulated by the Monetary Authority of Singapore under Singapore laws which differ from Chilean laws.

The afore-mentioned entities are hereinafter collectively referred to as Eastspring Investments.

The views and opinions contained herein are those of the author, and may not necessarily represent views expressed or reflected in other Eastspring Investments’ communications. This document is solely for information purposes and does not have any regard to the specific investment objective, financial situation and/or particular needs of any specific persons who may receive this document. This document is not intended as an offer, a solicitation of offer or a recommendation, to deal in shares of securities or any financial instruments. It may not be published, circulated, reproduced or distributed without the prior written consent of Eastspring Investments. Reliance upon information in this document is at the sole discretion of the reader. Please carefully study the related information and/or consult your own professional adviser before investing.

Investment involves risks. Past performance of and the predictions, projections, or forecasts on the economy, securities markets or the economic trends of the markets are not necessarily indicative of the future or likely performance of Eastspring Investments or any of the funds managed by Eastspring Investments.

Information herein is believed to be reliable at time of publication. Data from third party sources may have been used in the preparation of this material and Eastspring Investments has not independently verified, validated or audited such data. Where lawfully permitted, Eastspring Investments does not warrant its completeness or accuracy and is not responsible for error of facts or opinion nor shall be liable for damages arising out of any person’s reliance upon this information. Any opinion or estimate contained in this document may subject to change without notice.

Eastspring Investments companies (excluding joint venture companies) are ultimately wholly owned/indirect subsidiaries of Prudential plc of the United Kingdom. Eastspring Investments companies (including joint venture companies) and Prudential plc are not affiliated in any manner with Prudential Financial, Inc., a company whose principal place of business is in the United States of America or with the Prudential Assurance Company Limited, a subsidiary of M&G plc (a company incorporated in the United Kingdom).