Executive Summary

- Exchange offers are expanding the investable Asian credit universe, providing investors more ways to access the market.

- Exchange offers enable investors to adapt portfolios more dynamically as markets and issuer fundamentals shift.

- Navigating the complexities of exchange offers are critical for capturing yield and managing risks effectively.

Exchange offers present a compelling opportunity for bond investors who can navigate complexity and uncover relative value across issuers, structures, and maturities—thereby broadening the universe of investable bonds. These offers are being driven by a growing need among bond issuers to manage their liabilities more proactively. Liability management exercises (“LME”) form a critical strategic function that helps bond issuers enhance financial flexibility, optimise capital structure, manage market volatility, and pre-empt formal restructuring.

Among the various liability management tools, exchange offers are increasingly common. They involve swapping existing bonds for new ones, often with revised terms such as principal, coupon, maturity, or covenants—allowing issuers to reduce refinancing risks and better align debt obligations with future cash flows. Exchange offers tend to increase when market conditions turn challenging such as slower economic growth pressuring company profits, and tighter financing liquidity making traditional bond issuance less viable.

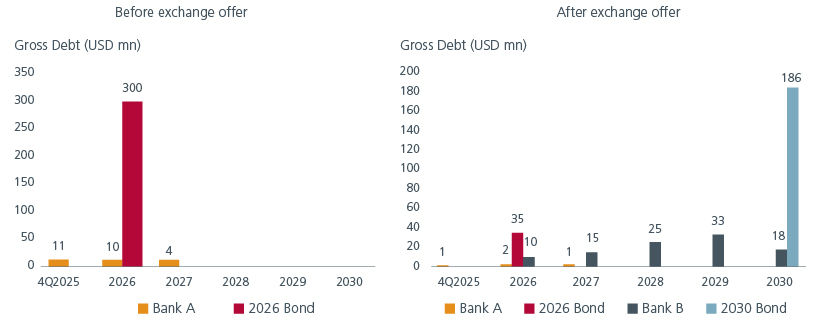

Fig 1: Hypothetical debt maturity profile of an issuer pre and post a bond exchange offer

Source: Eastspring Investments

Exchange offers are no longer niche—they are becoming a mainstream tool for both investment grade and high yield bond issuers.

Tapping the credit opportunities

While exchange offers have traditionally been a part of the Asian credit markets for bond issuers to manage their liability profiles, over the past two years, there has been a proliferation of various types of exchange offers across various Asian bond issuers, which vary in size and complexity. Over the past 10 years, there have been eleven investment grade, and nine high yield exchange offers.

Across Asia, there has also been pro-active liability management by higher quality Chinese industrial issuers, Indian corporates, and non-bank finance companies (NBFCs), as well as Philippine corporates, in line with constructive capital market conditions as investors reinvest maturing bond proceeds into new bond issues.

In an exchange offer, the promise by the issuer to pay the new debt obligation may have changed substantially from the original payment terms under the existing bond. This affects the evaluation of the issuer’s capacity, character, collateral, and covenants underpinning the repayment of the new debt obligation. Accordingly, a robust credit analysis is critical to identifying idiosyncratic credit opportunities and tail risk management.

Yield-hunting opportunities present themselves in terms of both curve plays (i.e. short-dated bonds versus long-dated bonds) and across USD versus local currency bond markets for Asian issuers on a currency-hedged basis, as credit conditions and currency basis evolve. These trends suggest that bond managers with regional expertise and access to local currency bond markets (e.g., IDR bonds) may be better positioned to capture yield opportunities and manage risk.

Navigating exchange offers demands expertise

While most exchange offers for investment grade bonds are fairly administrative and are consensual processes between the issuer and bond investors, the approach towards exchange offers for high yield bonds is differentiated by requiring a higher degree of active management. This often includes negotiations of key terms before an exchange offer is launched in a consensual process, especially for investors who have significant holdings in the bond and can elect to agree or disagree to the proposed changes by the issuer.

For investment grade and stronger high yield bond issuers in the JP Morgan Asia Credit Index, vanilla exchange offers pose the question of whether relative value is attractive enough for a simple maturity extension via participation in an exchange offer. However, for the lower-rated segment of high yield bond issuers, the ability to discern liquidity options for these high yield issuers and the evaluation of the specific structure of the exchange offer is not only key to managing idiosyncratic credit risks, it can also be a source of returns in determining which bonds have the greatest potential for yield compression as the likelihood of repayment increases.

Understanding the risks behind the opportunity

While exchange offers can broaden the investable universe and unlock relative value, they also demand careful evaluation due to structural risks that may weaken bondholder protections. Some issuers’ tactics include moving valuable assets to entities outside of the bond’s covenant protections (drop-down financings), restructuring debt in ways that disadvantage non-participating holders (up-tiering), and giving new bondholders multiple claims on the same assets (double-dip structures).

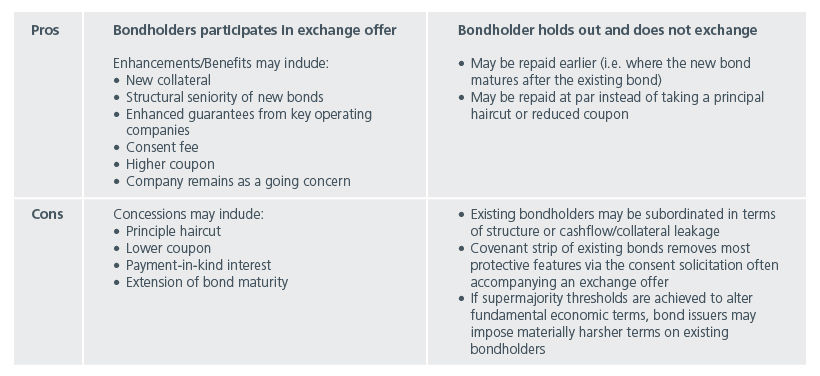

Beyond deal mechanics, investors must also weigh strategic considerations—such as holdout risks, the impact of unsuccessful offers, and the use of exit consents (see Fig. 2). Each scenario can affect credit quality, recovery prospects, and portfolio positioning. Ultimately, not all exchange offers are credit-positive, and bottom-up credit assessment remains essential to identifying which deals offer genuine upside versus hidden risks. In this way, expertise in deal structure and issuer fundamentals becomes a key source of alpha.

Fig 2: Implications of participating in an exchange offer

Source: Eastspring Investments

Why LME execution matters for credit selection

A quick walk down memory lane for the Asian aviation sector illustrates the aforementioned concepts in our credit selection. The outbreak of Covid-19 posed major operational and financial challenges for the aviation sector as air travel came to a halt. We highlight two flag carriers in the region that faced severe financial stress but took different approaches to liability management, resulting in divergent outcomes for investors.

One of them had strong state-linked shareholder support and hence received substantial liquidity infusions through equity, quasi-equity, and standby facilities. This support stabilised its balance sheet, maintained leverage ratios, and allowed the airline to refinance high-cost debt with new, lower-cost bonds as market conditions improved. The airline’s ability to repay debt in full and even ahead of schedule validated our investment thesis and delivered positive returns for investors.

In contrast, the other airline underwent multiple rounds of debt restructuring over the years, including principal haircuts, debt-for-equity swaps, coupon reductions, and tenor extensions. These measures resulted in significant net present value losses for investors. Persistent issues such as aggressive accounting practices and weak corporate governance further undermined confidence. Despite remaining in the JP Morgan Asia Credit Index, the airline is viewed cautiously due to its ongoing negative equity and uncertain repayment prospects.

The contrasting outcomes underscore the importance of rigorous, bottom-up credit assessment and issuer selection in extracting alpha from LMEs. Successful participation depends on selecting issuers with robust fundamentals and credible support, while steering clear of those with weak structures and governance issues.

Interesting reads

Singapore by Eastspring Investments (Singapore) Limited (UEN: 199407631H)

Australia (for wholesale clients only) by Eastspring Investments (Singapore) Limited (UEN: 199407631H), which is incorporated in Singapore, is exempt from the requirement to hold an Australian financial services licence and is licensed and regulated by the Monetary Authority of Singapore under Singapore laws which differ from Australian laws

Hong Kong by Eastspring Investments (Hong Kong) Limited and has not been reviewed by the Securities and Futures Commission of Hong Kong.

Indonesia by PT Eastspring Investments Indonesia, an investment manager that is licensed, registered and supervised by the Indonesia Financial Services Authority (OJK).

Malaysia by Eastspring Investments Berhad (200001028634/ 531241-U) and Eastspring Al-Wara’ Investments Berhad (200901017585 / 860682-K) and has not been reviewed by Securities Commission of Malaysia.

Thailand by Eastspring Asset Management (Thailand) Co., Ltd.

United States of America (for institutional clients only) by Eastspring Investments (Singapore) Limited (UEN: 199407631H), which is incorporated in Singapore and is registered with the U.S Securities and Exchange Commission as a registered investment adviser.

European Economic Area (for professional clients only) and Switzerland (for qualified investors only) by Eastspring Investments (Luxembourg) S.A., 26, Boulevard Royal, 2449 Luxembourg, Grand-Duchy of Luxembourg, registered with the Registre de Commerce et des Sociétés (Luxembourg), Register No B 173737.

Chile (for institutional clients only) by Eastspring Investments (Singapore) Limited (UEN: 199407631H), which is incorporated in Singapore and is licensed and regulated by the Monetary Authority of Singapore under Singapore laws which differ from Chilean laws.

The afore-mentioned entities are hereinafter collectively referred to as Eastspring Investments.

The views and opinions contained herein are those of the author, and may not necessarily represent views expressed or reflected in other Eastspring Investments’ communications. This document is solely for information purposes and does not have any regard to the specific investment objective, financial situation and/or particular needs of any specific persons who may receive this document. This document is not intended as an offer, a solicitation of offer or a recommendation, to deal in shares of securities or any financial instruments. It may not be published, circulated, reproduced or distributed without the prior written consent of Eastspring Investments. Reliance upon information in this document is at the sole discretion of the reader. Please carefully study the related information and/or consult your own professional adviser before investing.

Investment involves risks. Past performance of and the predictions, projections, or forecasts on the economy, securities markets or the economic trends of the markets are not necessarily indicative of the future or likely performance of Eastspring Investments or any of the funds managed by Eastspring Investments.

Information herein is believed to be reliable at time of publication. Data from third party sources may have been used in the preparation of this material and Eastspring Investments has not independently verified, validated or audited such data. Where lawfully permitted, Eastspring Investments does not warrant its completeness or accuracy and is not responsible for error of facts or opinion nor shall be liable for damages arising out of any person’s reliance upon this information. Any opinion or estimate contained in this document may subject to change without notice.

Eastspring Investments companies (excluding joint venture companies) are ultimately wholly owned/indirect subsidiaries of Prudential plc of the United Kingdom. Eastspring Investments companies (including joint venture companies) and Prudential plc are not affiliated in any manner with Prudential Financial, Inc., a company whose principal place of business is in the United States of America or with the Prudential Assurance Company Limited, a subsidiary of M&G plc (a company incorporated in the United Kingdom).