Summary

Asia ex Japan (“Asian”) equities are pricing in low expectations and limited investor appetite, after significant earnings and price underperformance as an asset class over the last decade. A rising rate cycle, delayed Covid-19 re-opening versus the West, and cash-rich balance sheets provide a good pathway to grow out of this underperformance. The ongoing supply chain diversification and decarbonisation cycle provide medium-term growth visibility. At current discounted valuations, we believe it is time to revisit the investment case for Asian equities.

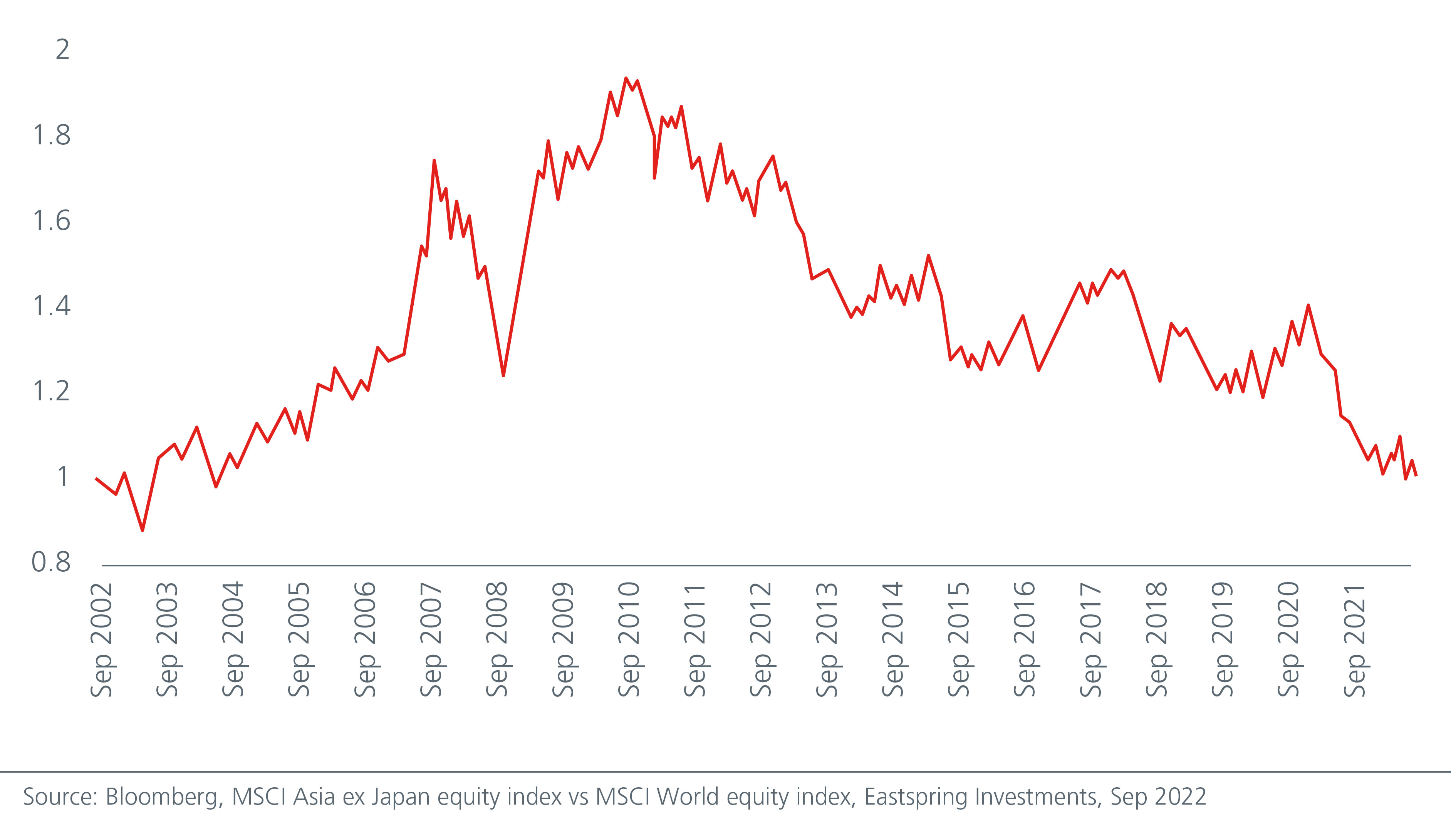

Asian equity indices have lagged their global peers by a wide margin over the last decade due to a lack of earnings per share growth, rising equity risk premium due to geopolitics and regulation, higher exposure to emission-sensitive industries and more recently, slower re-opening post Covid-19. See Fig 1. Unsurprisingly, global investors’ interest in Asian equities has declined considerably over this time. This is quite contrary to the market expectations 10 years ago on Asia’s growth, demographic and innovation potential.

Fig 1: Asia ex Japan equities lagged world equities over the last decade

We find the above market indifference on Asian equities among global investors has led to low expectations and light positioning in many Asian stocks. While the investment attributes and thesis around Asia’s middle-class income growth, innovation and exports have not changed compared to the last decade, expectations and the starting point for valuations are different. At the current 1.5x trailing price-to-book ratio, Asia currently trades at a 65% discount to MSCI US compared to 30% discount in 2012.1

This investment environment is steering us to an attractive list of good businesses at cheap valuations. We believe many of these businesses have been wrongly thrown out with the bath water, creating the mispricing we can exploit as an investment team. We find these businesses have a few common characteristics:

- Price and valuation de-rating have been driven by concerns on growth, regulation, or sustainable returns

- Medium-term sustainable returns that are higher than today’s expectations

- Management change, balance sheet repair or industry structure, suggesting a path to achieving these sustainable returns over a 3–5-year period

Earnings growth post the ongoing reset has credible drivers

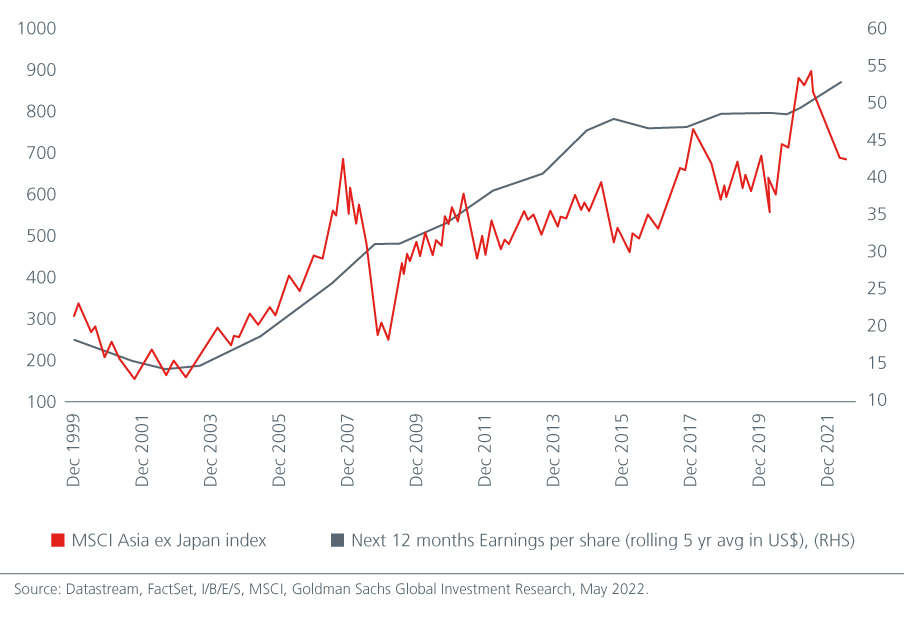

Earnings expectations have been in continuous decline this year, with almost all countries and sectors seeing broad cuts. With central banks tightening monetary policy to tame inflation, market expectations have come down for Asia too. Asia however is yet to see the Covid-19 re-opening benefits in North Asia (delayed compared to the rest of the World) which provides better visibility going into next year. See Fig 2. Moreover, Asian markets have a larger weight of financials among listed equities and the higher rates provide an earnings tailwind after years of yield compression.

Fig 2: Asia ex-Japan earnings versus the market index

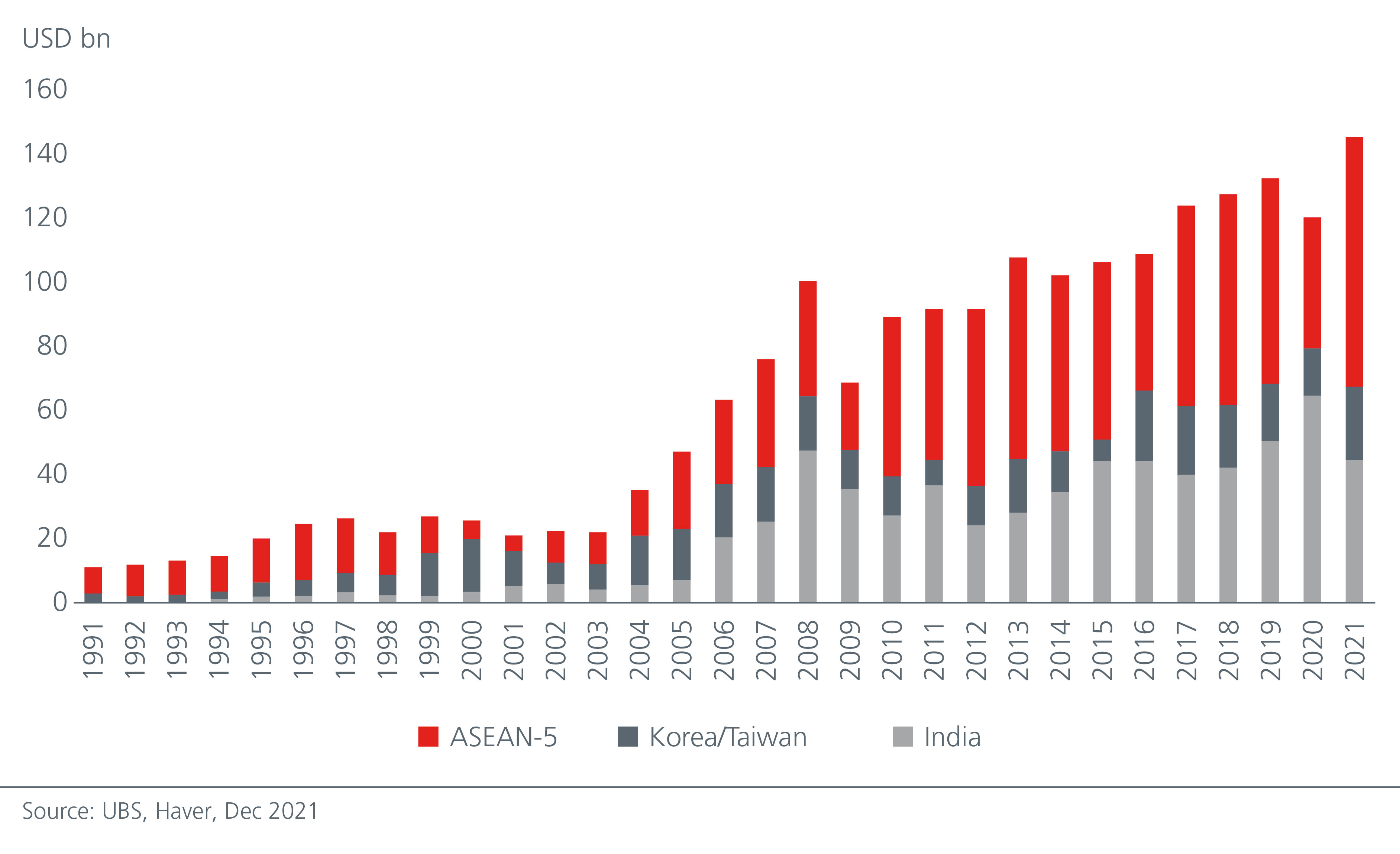

A key theme in recent years has been the diversification of global supply chains out of China, mostly into the rest of Asia. The prime beneficiaries have been Vietnam, India, and Indonesia. See Fig 3. Many Asian corporates from battery makers to semiconductors are also leading this supply chain diversification. This in our view adds to the earnings growth potential for Asia in the medium term.

Fig 3: Rising trend of inward FDI in Asia ex-China

Similarly Asian companies are increasingly recognising the need to step up on ESG investments and disclosures. In the medium term, the higher decarbonisation capex in Asia (delayed versus Europe who started the transition earlier) has the potential to add to earnings growth and quality. At the same time, the high levels of cash offer many Asia ex Japan companies a level of flexibility in funding these investments in supply chain diversification and decarbonisation despite the rising cost of capital; almost 45% of Asia ex Japan non-financial companies have net cash on their balance sheets vis-à-vis 23% of US counterparts.2

Asian indices are fairly diversified

The recent media coverage around geopolitics and investment risks in China has added to global investors’ concerns on investing in Asia. While this offers an opportunity to evaluate previously expensive but attractive Chinese businesses, there are plenty of earnings opportunities in Asian countries with growth drivers that are uncorrelated to China.

Nonetheless we are cognisant of the macro concerns and continuously analyse portfolio sensitivity to macroeconomic variables and unintended portfolio risks. At the portfolio construction stage, we set high return hurdles on stocks where reversion to intrinsic value is highly dependent or sensitive to macroeconomic outcomes including cost of capital, geopolitical improvement, and regulation. At the portfolio review stage, the focus is to maximise intended stock-specific risk, while minimising all unintended portfolio risks.

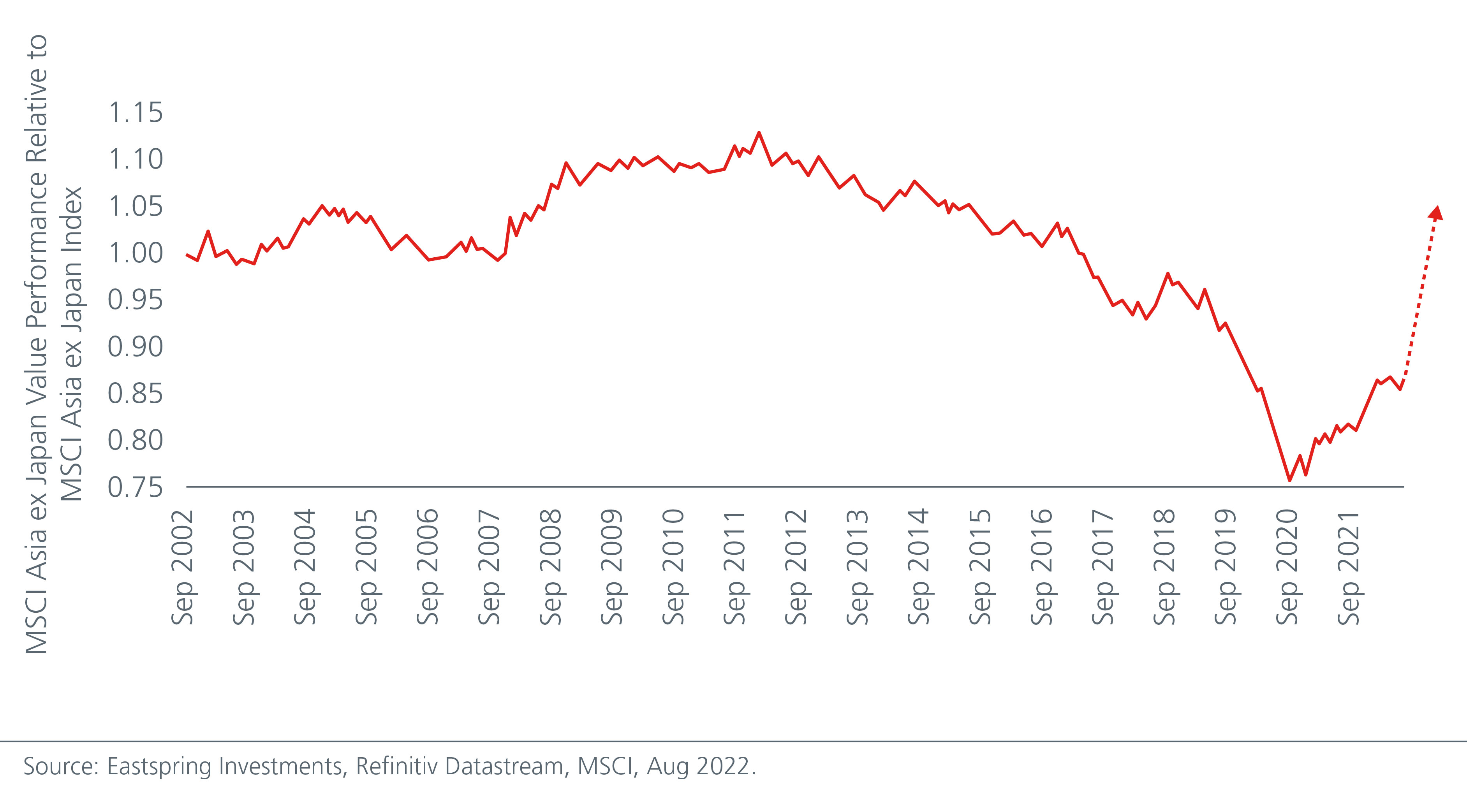

Supportive style tailwinds

We are also believers in the ongoing strategic shifts around decarbonisation, diversified supply chains and the higher cost of doing business. As shared in an earlier article (Value investing in Asia: A multi-year opportunity ), we are confident the resulting economic cycle from these strategic shifts is supportive of value’s continuing outperformance in Asia. See Fig 4.

Fig 4: Value style looks set to continue its outperformance

Time to re-evaluate Asian equity allocations

In summary, we believe it is time to revisit the investment case for Asian equities. The starting valuation for Asian equities is at a hefty discount to its own history and global peers, global investor crowding in this asset class is limited, geopolitics and regulatory concerns are no longer a surprise, and earnings expectations are ongoing a low reset.

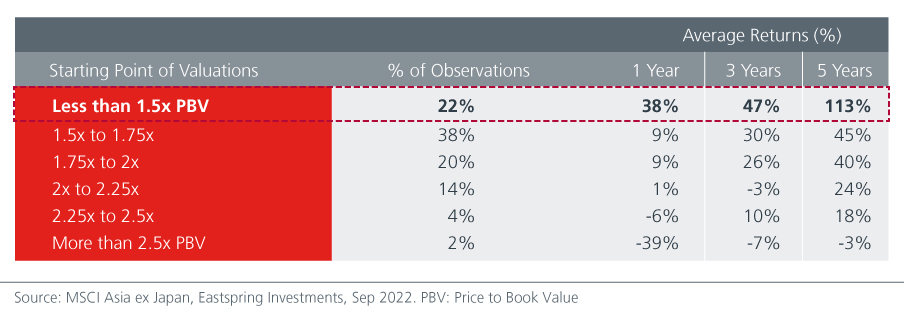

Back-testing historical returns in Asia ex Japan shows impressive returns over a 1/3/5 year investing horizon when the starting point of valuation is below the trailing price-to-book ratio of 1.5x. See Fig 5.

A rising rate cycle, delayed Covid-19 re-opening versus the West, ongoing supply chain diversification and decarbonisation investments provide a medium-term growth opportunity to recover the underperformance over the last decade. At this point, we believe the geographic and style allocations over the last few years and investor indifference to Asia should get re-evaluated.

Fig 5: Starting valuations matter

Interesting reads

Sources:

1 Bloomberg MSCI, Eastspring Investments, Sep 2022

2 “Cash rich” companies: Nomura, as at 15 August 2022. Companies’ ratio is the number of positive net cash companies divided by the number of index composite companies.

Singapore by Eastspring Investments (Singapore) Limited (UEN: 199407631H)

Australia (for wholesale clients only) by Eastspring Investments (Singapore) Limited (UEN: 199407631H), which is incorporated in Singapore, is exempt from the requirement to hold an Australian financial services licence and is licensed and regulated by the Monetary Authority of Singapore under Singapore laws which differ from Australian laws

Hong Kong by Eastspring Investments (Hong Kong) Limited and has not been reviewed by the Securities and Futures Commission of Hong Kong.

Indonesia by PT Eastspring Investments Indonesia, an investment manager that is licensed, registered and supervised by the Indonesia Financial Services Authority (OJK).

Malaysia by Eastspring Investments Berhad (531241-U).

Thailand by Eastspring Asset Management (Thailand) Co., Ltd.

United States of America (for institutional clients only) by Eastspring Investments (Singapore) Limited (UEN: 199407631H), which is incorporated in Singapore and is registered with the U.S Securities and Exchange Commission as a registered investment adviser.

European Economic Area (for professional clients only) and Switzerland (for qualified investors only) by Eastspring Investments (Luxembourg) S.A., 26, Boulevard Royal, 2449 Luxembourg, Grand-Duchy of Luxembourg, registered with the Registre de Commerce et des Sociétés (Luxembourg), Register No B 173737.

Chile (for institutional clients only) by Eastspring Investments (Singapore) Limited (UEN: 199407631H), which is incorporated in Singapore and is licensed and regulated by the Monetary Authority of Singapore under Singapore laws which differ from Chilean laws.

The afore-mentioned entities are hereinafter collectively referred to as Eastspring Investments.

The views and opinions contained herein are those of the author, and may not necessarily represent views expressed or reflected in other Eastspring Investments’ communications. This document is solely for information purposes and does not have any regard to the specific investment objective, financial situation and/or particular needs of any specific persons who may receive this document. This document is not intended as an offer, a solicitation of offer or a recommendation, to deal in shares of securities or any financial instruments. It may not be published, circulated, reproduced or distributed without the prior written consent of Eastspring Investments. Reliance upon information in this document is at the sole discretion of the reader. Please carefully study the related information and/or consult your own professional adviser before investing.

Investment involves risks. Past performance of and the predictions, projections, or forecasts on the economy, securities markets or the economic trends of the markets are not necessarily indicative of the future or likely performance of Eastspring Investments or any of the funds managed by Eastspring Investments.

Information herein is believed to be reliable at time of publication. Data from third party sources may have been used in the preparation of this material and Eastspring Investments has not independently verified, validated or audited such data. Where lawfully permitted, Eastspring Investments does not warrant its completeness or accuracy and is not responsible for error of facts or opinion nor shall be liable for damages arising out of any person’s reliance upon this information. Any opinion or estimate contained in this document may subject to change without notice.

Eastspring Investments companies (excluding joint venture companies) are ultimately wholly owned/indirect subsidiaries of Prudential plc of the United Kingdom. Eastspring Investments companies (including joint venture companies) and Prudential plc are not affiliated in any manner with Prudential Financial, Inc., a company whose principal place of business is in the United States of America or with the Prudential Assurance Company Limited, a subsidiary of M&G plc (a company incorporated in the United Kingdom).