Executive Summary

- SGD bonds serve as a high‑quality portfolio diversifier and balance‑sheet hedge, remaining relatively resilient during periods of market stress, including the current war‑related uncertainty.

- As developed markets’ fiscal risks rise, SGD bonds offer more reliable income with lower downside risk.

- With fundamentals intact, SGD bond returns will likely be driven by valuation and volatility, favouring an actively managed approach.

1. Do Singapore bonds continue to have a strategic role in portfolios today?

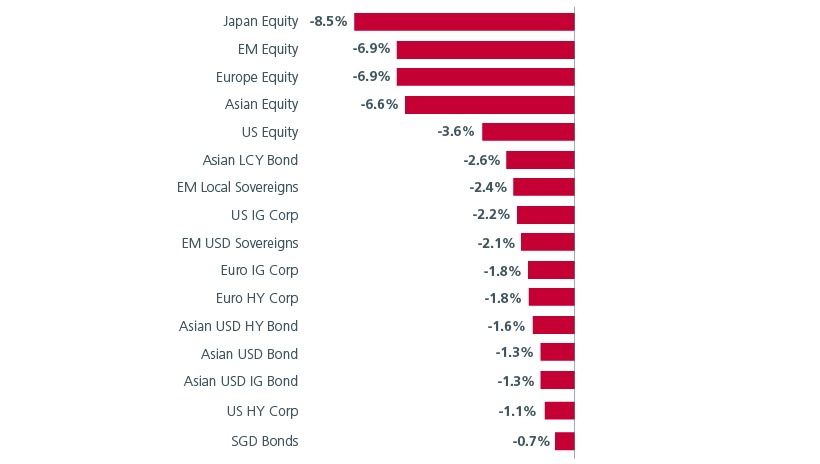

Despite heightened geopolitical uncertainty following the Iran conflict, month-to-date1 benchmark returns show that SGD bonds have held up better through the war‑related sell‑offs, with shallower declines than most other bond markets, including US bonds.

Fig 1: Singapore bonds show relative resilience amid current market sell-offs

Source: Markit IBOXX Singapore Bond TRI, ICE BAML US HY Corp, JACI Investment Grade, JACI Composite, JACI Non-Investment Grade, ML Europe HY Corp, ML Europe IG Corp, EMBI Global Diversified, ICE BAML US IG Corp, GBI-EM Local, Markit iBoxx ALBI, S&P 500, MSCI AC Asia Pac ex Japan (LCY), DJ Euro Stoxx 50, MSCI Emerging Markets (LCY), Nikkei 225, as of 13 March 2026

As such, Singapore bonds are increasingly well positioned as a strategic allocation in investor portfolios, particularly as demand for high‑quality, non‑USD safe‑haven assets continues to rise. Singapore dollar (SGD) bonds have attracted sustained global inflows, underpinned by their meaningful diversification benefits and consistently low correlation with broader risk assets. From a portfolio‑construction perspective, their relatively lower volatility profile can help support more stable portfolio outcomes and potentially improve a portfolio’s risk-return profile across market cycles

Fig 2: SGD bonds offer diversification benefits within multi asset portfolios

Source: Bloomberg as at 28 Feb 2026 based on 10-year monthly correlation data. Singapore Bonds represented by Markit iBoxx ALBI Singapore (SGD), 10Y US Treasury represented by the generic 10Y US Treasury Note futures, Asian USD Bonds represented by the JP Morgan Asia Credit Index (USD), Asia ex-Japan Equities represented by MSCI AC Asia ex Japan (USD), Singapore Equities represented by MSCI Singapore Index (SGD).

Importantly, SGD bonds can potentially be a complementary allocation in global portfolios. US Treasuries continue to serve as the world’s primary risk‑free asset and tactical risk‑off tool. Singapore government bonds too serve a similar role: a high‑quality (AAA‑rated) sovereign bond which is a portfolio diversifier and strong balance‑sheet hedge during periods of market stress.

SGD bonds (both sovereign and corporate) are better positioned as income generating capital‑preservation assets, particularly at a time when global fiscal sustainability is under increasing scrutiny. Income consistency is becoming more valuable and exposure to investment‑grade SGD bonds has the potential to deliver steady income with less downside risk.

This distinction has become more pronounced amid rising concerns over developed markets’ fiscal sustainability. With US President Trump likely to pursue expansionary policies ahead of the November mid‑term elections, the US’ projected FY2026 fiscal deficit of around US$1.9 trillion (~5.8% of GDP), suggests heavy Treasury supply, greater long‑end issuance and a steeper yield curve.

Against this backdrop, US Treasuries are likely to experience heightened volatility. By contrast, Singapore is expected to post a fiscal surplus of around S$8.5bn (~ 1% of GDP) in 2026, limiting supply pressures and helping to anchor bond yields and volatility, and thereby reinforcing the role of Singapore bonds as a stabilising force within global portfolios.

2. How compelling are Singapore government bonds relative to other bond markets?

2025 was a standout year for SGD government bonds. Falling SGD government yields, set against a backdrop of rising long‑end yields across several G3 markets, drove strong performance. This rally coupled with spread compression of SGD corporate bonds, however, raises questions on whether SGD bonds remain attractive.

When considering valuations, it is important to adjust yields to make it an apples-to-apples comparison. While Singapore bond yields may seem low on a nominal basis, they are considered fair to regional and global peers after adjusting for their cross-currency basis.

Market liquidity further reinforces Singapore bonds’ relative appeal. The SGD bond market is consistently recognised as one of the most developed and liquid in Asia, underpinned by deep and stable domestic institutional demand as well as robust retail participation. In contrast, many regional local currency bond markets are more sensitive to foreign flows, currency fluctuations and tend to experience sharper sell‑offs during risk‑off episodes.

Overall, the case for Singapore bonds rests on high credit quality and a favourable risk-return profile, which positions Singapore bonds as a high‑quality anchor within regional and global portfolios. Looking ahead, Singapore’s political stability and prudent fiscal and monetary policies should support steady performance in 2026, although returns are likely to normalise to around 2.5%–3.5%, following the exceptional 7%–8% gains (SGD terms) seen in 2025.

3. Which macro and policy drivers are likely to drive SGD bond returns?

Beyond fiscal discipline, the Monetary Authority of Singapore’s (MAS) monetary policy stance which is anchored on maintaining medium-term price stability is a key driver of SGD bond returns. To date, MAS has left policy settings unchanged, maintaining the slope of the SGD Nominal Effective Exchange Rate (NEER) policy band at 0.5% per annum.

From a policy perspective, MAS expects the output gap to remain positive, even as growth normalises and moderates to 2–4% in 2026 after expanding 5% in 2025. Inflation remains well contained, although MAS recently raised its inflation forecast to 1%–2% from 0.5%–1.5%. While the outlook appears stable for now, upside growth surprises or renewed geopolitical shocks (sustained rise in energy price or supply-chain disruption amid military conflict in the Middle East) could still pose risks to the inflation trajectory.

The upward revision in inflation forecasts increases the likelihood of policy tightening as early as April. Any tightening will result in a stronger SGD, potentially attracting more increased capital inflows and a steeper SGD yield curve.

Separately, the US Fed’s rate moves in the coming months could influence risk sentiment and term premia. Nonetheless SGD bonds tend to respond more modestly to US Treasury moves and curve repricing is often more muted than in G3 markets. This makes SGD bonds more resilient during periods of sharp Fed‑driven volatility.

MAS operates a managed float regime for the SGD. The SGD is relatively controllable through direct interventions in the foreign exchange markets and bears a stable and predictable relationship with price stability as the final target of policy over the medium term. Barring material change to the macro fundamental outlook, MAS is expected to maintain an appreciating SGD policy. Coupled with a weaker USD outlook over the medium term to long term, there is potential for further upside via the exposure in SGD currency. SGD-based investors who already have USD exposure may want to consider hedging some of their USD exposure.

4. Where are the best opportunities across duration and SGD credits?

Balancing between the front-end of the rates curve which is at multi-year lows versus the longer end of the curve who holds more duration risk, we find the belly of the curve (3 to 7 years) to offer the most compelling value today, where investors are better compensated for duration risk. Our current view would change if valuations improve or macro conditions shift.

As for credits, we prefer statutory board bonds, as well as high quality financial and corporate bonds which have lagged the SGS rally. Statutory board bond spreads versus Singapore government bonds look attractive at current levels.

5. What are the main risks facing SGD bonds?

Risks are skewed toward higher volatility and valuation sensitivity rather than a deterioration in credit fundamentals. Spreads are tight in certain parts of the market, and wide in others. On balance, SGD spreads are probably fair to slightly wide.

A key point to note is that many SGD bonds continue to be unrated by international credit rating agencies. Hence it is important to have boots on the ground to carry out in-depth credit research. In addition, bond demand-supply mechanics and market technicals shape bond pricing and having long expertise in this market is a useful advantage. This reinforces the case for active duration and risk management.

Interesting reads

Sources:

1 As of 13 March 2026

Singapore by Eastspring Investments (Singapore) Limited (UEN: 199407631H)

Australia (for wholesale clients only) by Eastspring Investments (Singapore) Limited (UEN: 199407631H), which is incorporated in Singapore, is exempt from the requirement to hold an Australian financial services licence and is licensed and regulated by the Monetary Authority of Singapore under Singapore laws which differ from Australian laws

Hong Kong by Eastspring Investments (Hong Kong) Limited and has not been reviewed by the Securities and Futures Commission of Hong Kong.

Indonesia by PT Eastspring Investments Indonesia, an investment manager that is licensed, registered and supervised by the Indonesia Financial Services Authority (OJK).

Malaysia by Eastspring Investments Berhad (200001028634/ 531241-U) and Eastspring Al-Wara’ Investments Berhad (200901017585 / 860682-K).

Thailand by Eastspring Asset Management (Thailand) Co., Ltd.

United States of America (for institutional clients only) by Eastspring Investments (Singapore) Limited (UEN: 199407631H), which is incorporated in Singapore and is registered with the U.S Securities and Exchange Commission as a registered investment adviser.

European Economic Area (for professional clients only) and Switzerland (for qualified investors only) by Eastspring Investments (Luxembourg) S.A., 26, Boulevard Royal, 2449 Luxembourg, Grand-Duchy of Luxembourg, registered with the Registre de Commerce et des Sociétés (Luxembourg), Register No B 173737.

Chile (for institutional clients only) by Eastspring Investments (Singapore) Limited (UEN: 199407631H), which is incorporated in Singapore and is licensed and regulated by the Monetary Authority of Singapore under Singapore laws which differ from Chilean laws.

The afore-mentioned entities are hereinafter collectively referred to as Eastspring Investments.

The views and opinions contained herein are those of the author, and may not necessarily represent views expressed or reflected in other Eastspring Investments’ communications. This document is solely for information purposes and does not have any regard to the specific investment objective, financial situation and/or particular needs of any specific persons who may receive this document. This document is not intended as an offer, a solicitation of offer or a recommendation, to deal in shares of securities or any financial instruments. It may not be published, circulated, reproduced or distributed without the prior written consent of Eastspring Investments. Reliance upon information in this document is at the sole discretion of the reader. Please carefully study the related information and/or consult your own professional adviser before investing.

Investment involves risks. Past performance of and the predictions, projections, or forecasts on the economy, securities markets or the economic trends of the markets are not necessarily indicative of the future or likely performance of Eastspring Investments or any of the funds managed by Eastspring Investments.

Information herein is believed to be reliable at time of publication. Data from third party sources may have been used in the preparation of this material and Eastspring Investments has not independently verified, validated or audited such data. Where lawfully permitted, Eastspring Investments does not warrant its completeness or accuracy and is not responsible for error of facts or opinion nor shall be liable for damages arising out of any person’s reliance upon this information. Any opinion or estimate contained in this document may subject to change without notice.

Eastspring Investments companies (excluding joint venture companies) are ultimately wholly owned/indirect subsidiaries of Prudential plc of the United Kingdom. Eastspring Investments companies (including joint venture companies) and Prudential plc are not affiliated in any manner with Prudential Financial, Inc., a company whose principal place of business is in the United States of America or with the Prudential Assurance Company Limited, a subsidiary of M&G plc (a company incorporated in the United Kingdom).