Executive Summary

- Emerging Markets' (EM) earnings are entering their strongest multi-year upswing in a quarter century, driven by improved fundamentals and investor sentiment.

- Geopolitical risks have introduced near-term headwinds via higher energy prices, though the earnings momentum remains intact for now.

- As the fundamental re-rating of EM equities remains on track, investors with a multi-year horizon should find compelling value in the asset class.

For years, EM equities have faced criticism as an asset class. In 2025, however, a clear turning point emerged. MSCI EM equities rose 34%, comfortably outperforming the S&P 500’s 18% gain as EM share prices finally responded to a sharp improvement in fundamentals. Two tailwinds drove this acceleration. First, Artificial Intelligence (AI) related capital spending has lifted EM companies, especially in North Asia, as key suppliers to the global AI supply chain, with many already seeing earnings gains from “picks‑and‑shovels” exposure. Second, a benign commodity backdrop alongside China’s anti involution policies and firmer metals demand supported resource heavy markets such as Brazil and South Africa.

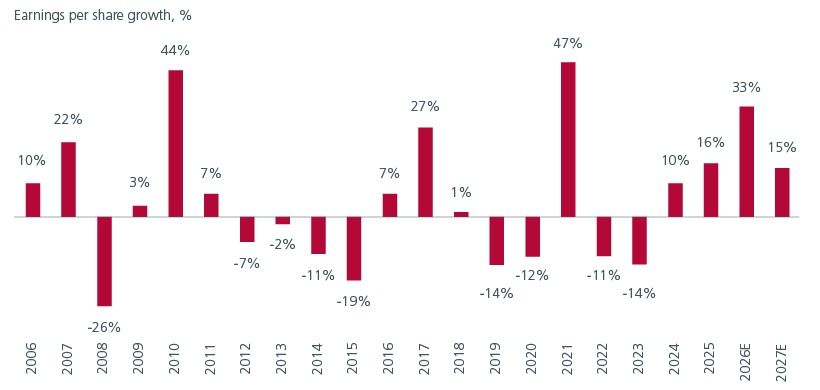

Consensus estimates now point to EM’s earnings per share (EPS) growth of 33% for 2026 and another 15% for 2027, building on solid 16% growth in 2025. See Fig 1. This would represent the strongest sustained earnings expansion in a quarter-century, unmatched except in recovery years following major shocks (e.g., 47% in 2021 post-COVID and 44% in 2010 after the Global Financial Crisis). The concern now is whether the higher energy prices arising from the US-Iran conflict could undermine this earnings momentum.

Fig 1: MSCI EM shows sustained earnings momentum

Source: Eastspring Investments, FactSet, Goldman Sachs, April 2026

Impact of Iran-US conflict

In a scenario of a prolonged conflict, with oil and gas prices remaining higher for longer, we should expect energy costs to feed through to broader inflation, triggering tighter monetary policies, and therefore, softer economic activity. Major energy importers, including India, Thailand, the Philippines, and Chile, face the most direct pressure. The United Arab Emirates and neighbouring countries, given geographic proximity, are also vulnerable to meaningful GDP impact. Net energy importers such as China, Korea, and Taiwan are likely to experience headwinds, though these could be mitigated by supportive fiscal policies and/or continued AI momentum.

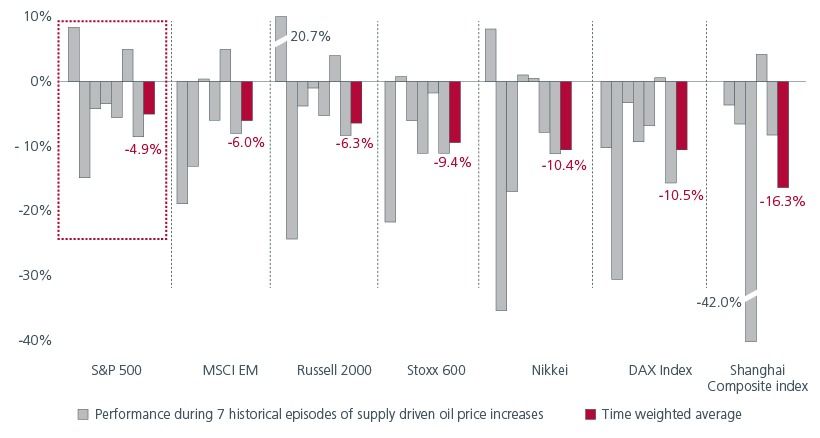

Interestingly, while the oil passthrough to inflation in each Emerging Market varies considerably, the region does not appear to be in a worse situation compared to most other Developed Markets (DM). In fact, when looking at the past supply-side oil shocks, MSCI EM Index has performed in line or better than S&P 500 and Stoxx 600 on most occasions. See Fig 2.

Fig 2: Equity markets’ performance during supply-side oil shocks

Source: Bloomberg, UBS. Note: a) The 7 historical episodes are i) Iranian Revolution ii) Gulf War iii) OPEC Supply Constraints iv) Venezuelan Oil Strike v) Outages in Venezuela, Iraq and Nigeria vi) Arab Spring and vii) Russian invasion; b) Time weighted average excludes Iranian Revolution; c) Shanghai Composite Index data not available for Iranian Revolution and Gulf War.

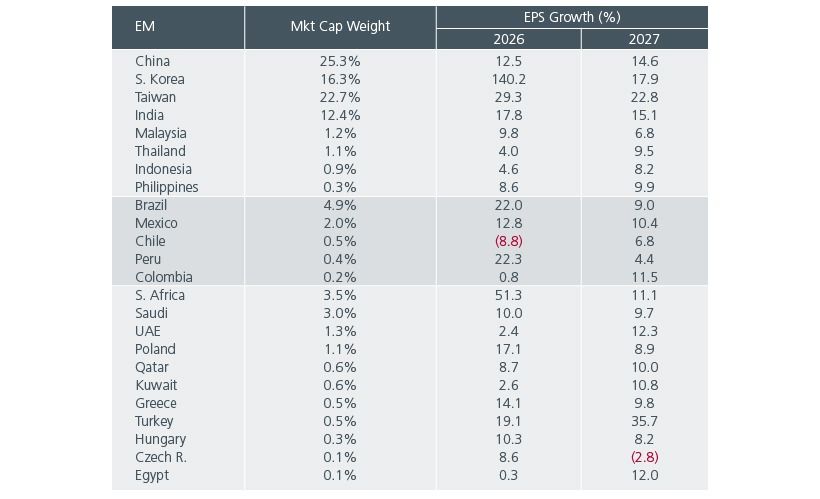

This suggests EM equities continue to be a good candidate for investors seeking diversification away from US equities. Most likely due to significant uncertainty, earnings forecasts remain unchanged for now, though a downward revision is likely in the coming quarters.

Fig 3: Earnings growth across EMs

Source: Eastspring Investments, IBES, J.P. Morgan, March 2026

The long-term case for EM equities remains intact

More than a month into the conflict, the outcome remains uncertain. While it is still too early to quantify the impact on EM, consensus expectations appear to be pricing in a relatively swift resolution, warranting some caution. Nonetheless, taking a longer-term perspective, the structural drivers supporting EM equities are unchanged and, in some cases, strengthened:

- Corporate governance reforms are gaining traction across key markets. This is a gradual process that should not be impacted by geopolitics. Over time, improved capital allocation should help narrow the gap between GDP and EPS growth. The US dollar moves in long cycles and trade-weighted USD appreciation trend in the last 15 years might have ended in 2025. While a knee-jerk reaction to war is usually USD appreciation, the structural factors driving a weaker greenback are not likely to change.

- Capex cycles historically favour EM equities. Increased global tensions might accelerate capex in AI, defense budgets, energy transition, and re-arrangement of supply chains.

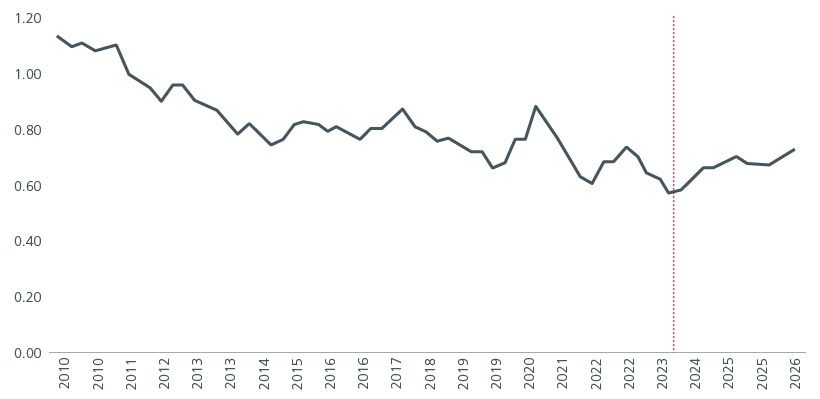

- In the past few years, Developed Market companies have benefited from asset-light structures and new business models with powerful network effects. As AI reshapes several industries, potentially disrupting moats, returns might be under pressure.

Fig 4: Returns on equity – MSCI EM relative to SPX Index

Source: Bloomberg, Eastspring Investments as of 20 April 2026

Interesting reads

Singapore by Eastspring Investments (Singapore) Limited (UEN: 199407631H)

Australia (for wholesale clients only) by Eastspring Investments (Singapore) Limited (UEN: 199407631H), which is incorporated in Singapore, is exempt from the requirement to hold an Australian financial services licence and is licensed and regulated by the Monetary Authority of Singapore under Singapore laws which differ from Australian laws

Hong Kong by Eastspring Investments (Hong Kong) Limited and has not been reviewed by the Securities and Futures Commission of Hong Kong.

Indonesia by PT Eastspring Investments Indonesia, an investment manager that is licensed, registered and supervised by the Indonesia Financial Services Authority (OJK).

Malaysia by Eastspring Investments Berhad (200001028634/ 531241-U) and Eastspring Al-Wara’ Investments Berhad (200901017585 / 860682-K).

Thailand by Eastspring Asset Management (Thailand) Co., Ltd.

United States of America (for institutional clients only) by Eastspring Investments (Singapore) Limited (UEN: 199407631H), which is incorporated in Singapore and is registered with the U.S Securities and Exchange Commission as a registered investment adviser.

European Economic Area (for professional clients only) and Switzerland (for qualified investors only) by Eastspring Investments (Luxembourg) S.A., 26, Boulevard Royal, 2449 Luxembourg, Grand-Duchy of Luxembourg, registered with the Registre de Commerce et des Sociétés (Luxembourg), Register No B 173737.

Chile (for institutional clients only) by Eastspring Investments (Singapore) Limited (UEN: 199407631H), which is incorporated in Singapore and is licensed and regulated by the Monetary Authority of Singapore under Singapore laws which differ from Chilean laws.

The afore-mentioned entities are hereinafter collectively referred to as Eastspring Investments.

The views and opinions contained herein are those of the author, and may not necessarily represent views expressed or reflected in other Eastspring Investments’ communications. This document is solely for information purposes and does not have any regard to the specific investment objective, financial situation and/or particular needs of any specific persons who may receive this document. This document is not intended as an offer, a solicitation of offer or a recommendation, to deal in shares of securities or any financial instruments. It may not be published, circulated, reproduced or distributed without the prior written consent of Eastspring Investments. Reliance upon information in this document is at the sole discretion of the reader. Please carefully study the related information and/or consult your own professional adviser before investing.

Investment involves risks. Past performance of and the predictions, projections, or forecasts on the economy, securities markets or the economic trends of the markets are not necessarily indicative of the future or likely performance of Eastspring Investments or any of the funds managed by Eastspring Investments.

Information herein is believed to be reliable at time of publication. Data from third party sources may have been used in the preparation of this material and Eastspring Investments has not independently verified, validated or audited such data. Where lawfully permitted, Eastspring Investments does not warrant its completeness or accuracy and is not responsible for error of facts or opinion nor shall be liable for damages arising out of any person’s reliance upon this information. Any opinion or estimate contained in this document may subject to change without notice.

Eastspring Investments companies (excluding joint venture companies) are ultimately wholly owned/indirect subsidiaries of Prudential plc of the United Kingdom. Eastspring Investments companies (including joint venture companies) and Prudential plc are not affiliated in any manner with Prudential Financial, Inc., a company whose principal place of business is in the United States of America or with the Prudential Assurance Company Limited, a subsidiary of M&G plc (a company incorporated in the United Kingdom).