Executive Summary

- Given Asia’s heterogeneity and wide return dispersion, active management is essential to access opportunities beyond indices.

- Structural information gaps across Asia allow active managers to add value through fundamental research and local insight.

- Rising concentration risk reinforces the case for active management to manage hidden risks and identify mispriced opportunities.

In highly efficient markets with deep liquidity, broad analyst coverage and rapid information dissemination, passive strategies can offer a cost‑effective way to capture market returns. But this logic weakens materially when applied to Asia.

Asia is not a single, homogenous investment environment. It is a mosaic of developed, emerging and frontier markets, each with distinct regulatory regimes, corporate governance standards, liquidity profiles, and investor bases.

The region’s equity markets are structurally different. Lower levels of real‑time information, price transparency and analyst coverage across many Asian markets have historically resulted in lower market efficiency, creating conditions where active management becomes essential.

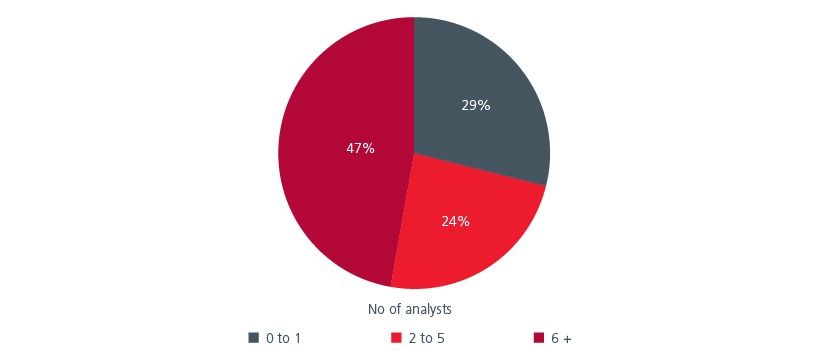

Asia remains under-researched

One of the most compelling arguments for active investing in Asia is the lack of comprehensive sell‑side coverage. Sizeable portions of ASEAN markets remain either lightly covered or entirely uncovered by analysts.

Fig 1. Share of ASEAN companies with analyst coverage

Source: Eastspring Investments, Bloomberg using the FTSE ASEAN All-Share Index as of 31 August 2025.

Limited coverage means that prices adjust more slowly to latest information. Corporate improvements, balance‑sheet repair, and/or governance changes are often underappreciated for extended periods. For investors willing to conduct bottom‑up research, this creates opportunities to identify mispriced assets well before they are recognised by the broader market.

This is a structural feature of Asian markets, not a cyclical one. As long as coverage remains uneven and information asymmetry persists, active managers retain the potential to add value through fundamental research and local insight.

Indices do not reflect Asia’s true opportunity set

Asia’s opportunity extends far beyond what is captured in major benchmarks. The region is home to a vast number of listed companies with domestic, regional and global relevance, many of which sit outside mainstream indices due to size, liquidity or classification constraints.

Furthermore, a breakdown of the MSCI AC Asia ex Japan index reveals that countries like China, Taiwan, and sectors such as Information Technology and Financials account for the bulk of the exposure. For investors, this means that buying “the market” often translates into owning a small number of popular names at elevated valuations, with limited exposure to the wider opportunity set.

Besides indices reflect what has already grown large, not what is in the process of becoming important. In Asia, where structural change, industrial upgrading and demographic shifts are ongoing, this lag is especially costly.

Active managers with on‑the‑ground presence are better positioned to identify emerging leaders early, before they enter index universes or attract broad investor attention. The ability of an asset manager to conduct on-the ground research of a market too opens access to stocks beyond what is available in an index. While this requires patience and an in depth understanding of each market’s nuances, the rewards can be handsome.

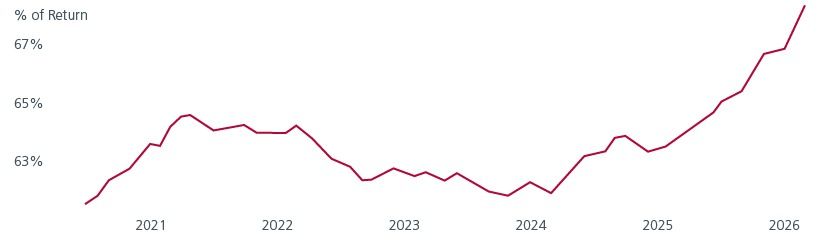

Concentration risk is growing

The assumption that an index represents the market is also becoming less valid. Larger companies, already prominent in the index, tend to receive more inflows, which pushes their valuations higher, thereby reinforcing their dominance in the index. The result is a market that is increasingly driven by a handful of names. Since 2024, the largest companies in the Asia ex Japan investment universe have increasingly driven the region’s performance.

Fig 2. Asia ex Japan universe* return contribution by the largest 5% of constituents

Source: Analysis window: 1 June 2020 to 27 February 2026. *Our proprietary Asia ex-Japan investment universe comprises stocks drawn from major indices—including S&P BMI Global, MSCI ACWI, MSCI Frontier, JCI, FTSE Bursa 100, among others (non-exhaustive). This universe is further refined to include only stocks listed in the following countries: Hong Kong, Singapore, China, India, Indonesia, South Korea, Malaysia, Philippines, Taiwan, Thailand, Bangladesh, Pakistan, Sri Lanka, and Vietnam.

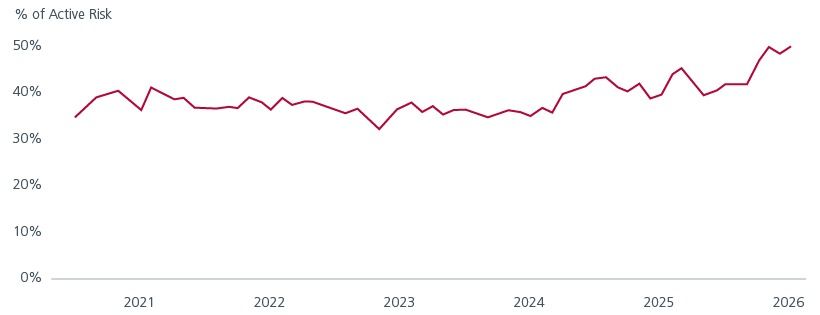

This concentration introduces real risk. When a few companies account for a disproportionate share of the index performance, any weakness in those names can potentially drag down an entire portfolio. The top 10 stocks in the MSCI AC Asia ex Japan Index now account for 50% of the index’s risk. Investors who thought they were buying “the market” are actually exposed to a narrow slice.

Fig 3. MSCI AC Asia ex Japan index - risk contribution by the largest 10 constituents

Source: Analysis window: 1 June 2020 to 27 February 2026. Axioma Fundamental Asia Pacific ex Japan Medium-Horizon.

Active is not optional in Asia

The case for active investing in Asia is fundamentally a structural one. Concentrated indices, uneven information flow, under‑researched markets, wide valuation dispersion, and complex policy dynamics combine to create an environment where passive strategies struggle to reflect underlying economic realities.

At the same time, the sheer breadth of opportunities is compelling. Asian equity markets offer several thousand stocks, spanning domestically focused companies as well as firms with regional and global exposure. Asia Pacific’s IPO markets also remain highly active. In 2025, the region recorded a 106% increase in IPO proceeds compared to 2024, with seven of the world’s top 10 global deals taking place in the region. India was the most active listing destination globally by deal count, registering a record 367 IPOs.1

In such a diverse market, active management offers an important advantage. Active managers can adjust portfolios dynamically in response to changing risks by reducing exposure to overheated segments, managing country allocations, and navigating periods of heightened volatility. In an environment where traditional correlations can break down and historical relationships no longer hold, flexibility becomes a critical advantage rather than a tactical choice.

For investors seeking to access Asia’s growth, innovation and diversification benefits, active management is not about chasing short‑term outperformance. It is about navigating complexity, avoiding hidden risks, and capturing opportunities that indices systematically miss. Against this backdrop, the case for active management for long-term investors in Asia has never been stronger.

Interesting reads

Sources:

1https://www.ey.com/en_sg/insights/ipo/trends

Singapore by Eastspring Investments (Singapore) Limited (UEN: 199407631H)

Australia (for wholesale clients only) by Eastspring Investments (Singapore) Limited (UEN: 199407631H), which is incorporated in Singapore, is exempt from the requirement to hold an Australian financial services licence and is licensed and regulated by the Monetary Authority of Singapore under Singapore laws which differ from Australian laws

Hong Kong by Eastspring Investments (Hong Kong) Limited and has not been reviewed by the Securities and Futures Commission of Hong Kong.

Indonesia by PT Eastspring Investments Indonesia, an investment manager that is licensed, registered and supervised by the Indonesia Financial Services Authority (OJK).

Malaysia by Eastspring Investments Berhad (200001028634/ 531241-U) and Eastspring Al-Wara’ Investments Berhad (200901017585 / 860682-K) and has not been reviewed by Securities Commission of Malaysia.

Thailand by Eastspring Asset Management (Thailand) Co., Ltd.

United States of America (for institutional clients only) by Eastspring Investments (Singapore) Limited (UEN: 199407631H), which is incorporated in Singapore and is registered with the U.S Securities and Exchange Commission as a registered investment adviser.

European Economic Area (for professional clients only) and Switzerland (for qualified investors only) by Eastspring Investments (Luxembourg) S.A., 26, Boulevard Royal, 2449 Luxembourg, Grand-Duchy of Luxembourg, registered with the Registre de Commerce et des Sociétés (Luxembourg), Register No B 173737.

Chile (for institutional clients only) by Eastspring Investments (Singapore) Limited (UEN: 199407631H), which is incorporated in Singapore and is licensed and regulated by the Monetary Authority of Singapore under Singapore laws which differ from Chilean laws.

The afore-mentioned entities are hereinafter collectively referred to as Eastspring Investments.

The views and opinions contained herein are those of the author, and may not necessarily represent views expressed or reflected in other Eastspring Investments’ communications. This document is solely for information purposes and does not have any regard to the specific investment objective, financial situation and/or particular needs of any specific persons who may receive this document. This document is not intended as an offer, a solicitation of offer or a recommendation, to deal in shares of securities or any financial instruments. It may not be published, circulated, reproduced or distributed without the prior written consent of Eastspring Investments. Reliance upon information in this document is at the sole discretion of the reader. Please carefully study the related information and/or consult your own professional adviser before investing.

Investment involves risks. Past performance of and the predictions, projections, or forecasts on the economy, securities markets or the economic trends of the markets are not necessarily indicative of the future or likely performance of Eastspring Investments or any of the funds managed by Eastspring Investments.

Information herein is believed to be reliable at time of publication. Data from third party sources may have been used in the preparation of this material and Eastspring Investments has not independently verified, validated or audited such data. Where lawfully permitted, Eastspring Investments does not warrant its completeness or accuracy and is not responsible for error of facts or opinion nor shall be liable for damages arising out of any person’s reliance upon this information. Any opinion or estimate contained in this document may subject to change without notice.

Eastspring Investments companies (excluding joint venture companies) are ultimately wholly owned/indirect subsidiaries of Prudential plc of the United Kingdom. Eastspring Investments companies (including joint venture companies) and Prudential plc are not affiliated in any manner with Prudential Financial, Inc., a company whose principal place of business is in the United States of America or with the Prudential Assurance Company Limited, a subsidiary of M&G plc (a company incorporated in the United Kingdom).