Wai Mei Leong

Portfolio Manager, Head of Credit,

Fixed Income,

Eastspring Investments

Apr 2023 | 5 min read

Summary

AT1s serve to strengthen a bank’s overall reserves and will thus remain a viable segment despite the dent in sentiment caused by the Credit Suisse debacle. Systemically important banks with AT1 exposures that have experienced improved capital and liquidity levels over the years should benefit from the flight to safety.

Investors are reassessing the risk inherent in bank instruments after the Swiss Financial Market Supervisory Authority (FINMA) wrote off USD17bn1 worth of Credit Suisse’s Additional Tier 1 (AT1) bonds under a bank rescue deal. It was a controversial move as regulators have chosen to favour shareholders to receive some compensation over AT1 holders who receive nothing. Under the “no creditor worse off” principle, equity holders would normally bear the brunt of write downs in a bank resolution scenario. Bond investors are thus left wondering if this sets a precedent for other regulators as the terms and conditions of most AT1s are similar.

Although other central banks i.e. Bank of England, the European Central Bank, Canada’s Office of the Superintendent of Financial Institutions and the monetary authorities in Singapore and Hong Kong reaffirmed their commitment to keep to the conventional creditor priority stance, the wider market implication of the Swiss move is uncertain. Still there is likely to be repricing of the AT1 market. Banks that rely more on AT1s may face more challenging conditions to raise capital. Having sufficient capital levels above the minimum regulatory requirements is therefore key in current market conditions.

Asian banks seem adequately capitalised

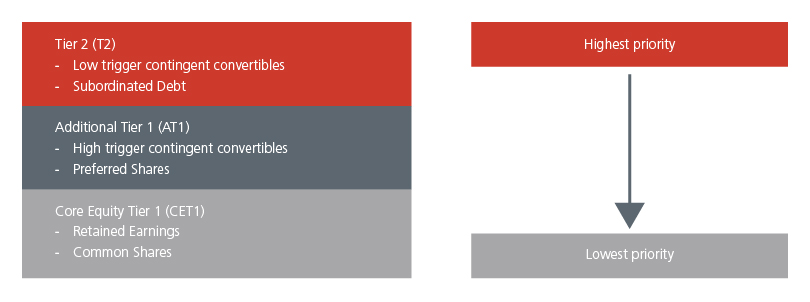

A bank’s loss absorption structure is made up of Tier 1 and Tier 2 capital. Core Equity Tier 1 (CET1) is considered as high-quality regulatory core capital that can be liquidated quickly to absorb losses. Additional Tier 1 capital (AT1) also provides a loss absorption feature but on a going-concern basis. Next comes Tier 2 which is expected to absorb losses before depositors and general creditors. See Fig 1. Together, Tier 1 and Tier 2 make up the total loss absorption capacity eligible liabilities of a bank.

As per the Basel III requirements, banks are required to maintain specified minimum levels of CET1, Tier 1 and total capital (Tier 1 + Tier 2), with each level calculated as a percentage of risk-weighted assets. The regulatory levels however differ across jurisdictions.

Fig 1: Seniority ranking of bank capital structure

Source: Bank of International Settlements and Eastspring Investments, April 2023

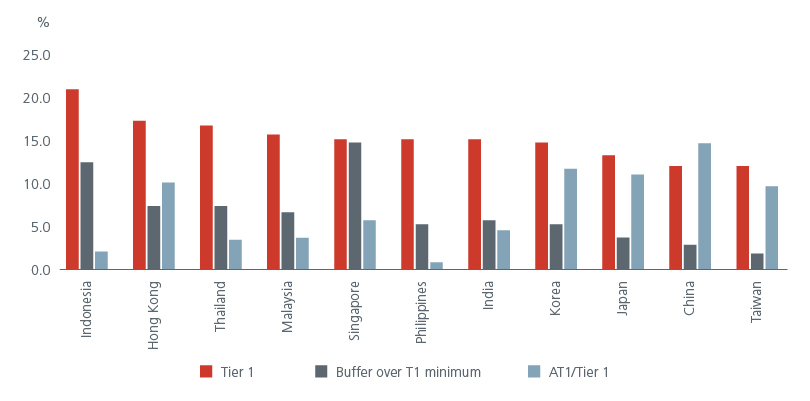

In general, Asian banks have maintained higher than regulated capital adequacy ratios; their Tier 1 ratios are mostly above 15%. See Fig 2. Post the 1997 Asian Financial Crisis (AFC), Asia embarked on financial and structural reforms which not only shored up bank capital but also reduced the financial sector’s leverage. This was a key reason the region was more resilient than many other parts of the world during the 2009 Global Financial Crisis (GFC). Although banks in North Asia tend to have a higher proportion of AT1s relative to CET1, the overall proportion across the region suggests that there is no significant reliance on AT1 capital.

Fig 2: Average Tier 1 ratios of select Asian banks

Source: Citigroup, Eaststpring Investments. Average of 18 CH banks, 2 HK banks, 3 SG banks, 3 PH banks, 5 MY banks, 3 JP banks, 12 IN banks, 3 KR banks, 5 TW banks, 4 ID banks, 6 TH banks based on data as at December 22

Largest Asian banks are not over leveraged

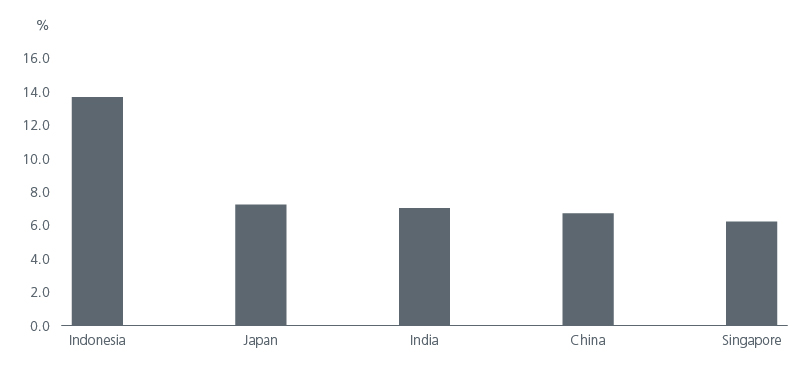

A leverage ratio is one of the several credit metrics used to assess a company’s financial strength. It reveals the degree to which a company’s operations are funded by debt. Typically, the higher the leverage ratios, the riskier the company. However, in the case of leverage ratios for banks it is the opposite.

Under the Basel III framework, banks are recommended to maintain a leverage ratio of more than 3%, a figure that is calculated by dividing a bank’s total Tier 1 capital over its average total consolidated assets. A higher ratio indicates that the bank can finance its assets with its equity and a higher likelihood of withstanding negative shocks. In Asia, the leverage ratios of the largest banks exceed 6%. See Fig 3.

Fig 3: Average leverage ratios of largest banks in Asia

Source: S&P Global, Eaststpring Investments. Average of 27 CH banks, 3 SG banks, 7 JP banks, 7 IN banks, 2 ID banks based on data as at Sep 22

Furthermore, the authorities in Asia have implemented various macroprudential measures to ensure the stability of the financial system post the AFC and GFC. These have served to reduce risk of bubbles especially in the property sector.

Asian regulators appear to be creditor friendly

Asian banks were naturally not spared when the recent contagion fears hit; their shares and bonds sold off but have since regained ground. More importantly the capital structures of Asian banks are under scrutiny. According to research firm Creditsights, a similar clause exists in Asian banks’ AT1 notes which can result in AT1s being written off or in some cases converted to equity.

We believe that Asian regulators are more creditor friendly. Back in 2009, when a Korean bank decided not to call their sub debt as it did not make economic sense for that bank, the Korean regulators pressured them to reverse the decision which helped shore investor confidence. Similarly, last November, a Korean life insurer had to reverse its decision to not call a USD perpetual note for economic reasons in a matter of days.

That said, in 2020, as part of the restructuring process of an Indian bank, the Reserve Bank of India wrote off the former’s entire AT1 debt. This underscores the importance of a prudent approach and thorough credit assessment of a bank’s capital structure. Non-call risks for AT1s will ultimately depend on the capital reserves and financing needs of the bank.

Where we see value

According to Financial Times,2 the size of the AT1 market is around USD 260 bn. This debt segment which was introduced post GFC strengthens a bank’s reserves and will likely remain a viable segment. Hence despite the current dent in sentiment for AT1s, we are overall not completely bearish on AT1s and will continue to look for opportunities based on a variety of credit metrics. As the valuations for AT1s had been tight prior to this incident, we generally preferred Tier 2 capital over AT1s, especially subordinated debt which we believe offers better risk reward outcomes. We are conscious of potential further AT1 repricing risk, extension risk and the end of the credit cycle.

Our AT1 exposures are mainly concentrated in global systemically important banks (G-SIBs) or national champions in favourable macroeconomic environments, where their capitalisation and liquidity have largely improved over the years, and these larger banks should benefit from flight to safety although confidence remains key.

Interesting reads

Sources:

1Bloomberg, 19 Mar 2023

2https://www.ft.com/content/47168c08-f09e-4ddb-905f-3c368c4f2b05

This document is produced by Eastspring Investments (Singapore) Limited and issued in:

Singapore by Eastspring Investments (Singapore) Limited (UEN: 199407631H)

Australia (for wholesale clients only) by Eastspring Investments (Singapore) Limited (UEN: 199407631H), which is incorporated in Singapore, is exempt from the requirement to hold an Australian financial services licence and is licensed and regulated by the Monetary Authority of Singapore under Singapore laws which differ from Australian laws

Hong Kong by Eastspring Investments (Hong Kong) Limited and has not been reviewed by the Securities and Futures Commission of Hong Kong.

Indonesia by PT Eastspring Investments Indonesia, an investment manager that is licensed, registered and supervised by the Indonesia Financial Services Authority (OJK).

Malaysia by Eastspring Investments Berhad (200001028634/ 531241-U) and Eastspring Al-Wara’ Investments Berhad (200901017585 / 860682-K) and has not been reviewed by Securities Commission of Malaysia.

Thailand by Eastspring Asset Management (Thailand) Co., Ltd.

United States of America (for institutional clients only) by Eastspring Investments (Singapore) Limited (UEN: 199407631H), which is incorporated in Singapore and is registered with the U.S Securities and Exchange Commission as a registered investment adviser.

European Economic Area (for professional clients only) and Switzerland (for qualified investors only) by Eastspring Investments (Luxembourg) S.A., 26, Boulevard Royal, 2449 Luxembourg, Grand-Duchy of Luxembourg, registered with the Registre de Commerce et des Sociétés (Luxembourg), Register No B 173737.

Chile (for institutional clients only) by Eastspring Investments (Singapore) Limited (UEN: 199407631H), which is incorporated in Singapore and is licensed and regulated by the Monetary Authority of Singapore under Singapore laws which differ from Chilean laws.

The afore-mentioned entities are hereinafter collectively referred to as Eastspring Investments.

The views and opinions contained herein are those of the author, and may not necessarily represent views expressed or reflected in other Eastspring Investments’ communications. This document is solely for information purposes and does not have any regard to the specific investment objective, financial situation and/or particular needs of any specific persons who may receive this document. This document is not intended as an offer, a solicitation of offer or a recommendation, to deal in shares of securities or any financial instruments. It may not be published, circulated, reproduced or distributed without the prior written consent of Eastspring Investments. Reliance upon information in this document is at the sole discretion of the reader. Please carefully study the related information and/or consult your own professional adviser before investing.

Investment involves risks. Past performance of and the predictions, projections, or forecasts on the economy, securities markets or the economic trends of the markets are not necessarily indicative of the future or likely performance of Eastspring Investments or any of the funds managed by Eastspring Investments.

Information herein is believed to be reliable at time of publication. Data from third party sources may have been used in the preparation of this material and Eastspring Investments has not independently verified, validated or audited such data. Where lawfully permitted, Eastspring Investments does not warrant its completeness or accuracy and is not responsible for error of facts or opinion nor shall be liable for damages arising out of any person’s reliance upon this information. Any opinion or estimate contained in this document may subject to change without notice.

Eastspring Investments companies (excluding joint venture companies) are ultimately wholly owned/indirect subsidiaries of Prudential plc of the United Kingdom. Eastspring Investments companies (including joint venture companies) and Prudential plc are not affiliated in any manner with Prudential Financial, Inc., a company whose principal place of business is in the United States of America or with the Prudential Assurance Company Limited, a subsidiary of M&G plc (a company incorporated in the United Kingdom).