Eastspring Investments

Apr 2026|5 min read

Executive Summary

- Special situations arise from temporary dislocations, where market sentiment turns overly negative despite underlying fundamentals remaining intact.

- India offers a particularly rich opportunity set, given its market depth, evolving corporate landscape, and transition-led mispricing.

- Special situations focus on resolution, assessing whether challenges are solvable and whether valuations adequately compensate for uncertainty.

Historically, information asymmetry was considered a key driver of alpha generation. However, with the widespread availability of information, markets worldwide, including those in India, have become much more efficient than they were a few decades ago. Yet, even in this era of transparency, inefficiencies persist. Are there blind spots in the market where superior fundamentals are overlooked, and where valuations remain misaligned with fundamentals? Special situations may create such opportunities.

Understanding special situations

Unlike what is commonly believed, special situations are not dependent on information asymmetry. Rather, identifying a special situation means assessing an investment thesis where the market’s response is overly negative to temporary, solvable challenges faced by a company, thus providing an opportunity to invest.

Special situations can stem from a variety of developments:

1. Company-specific (e.g. unpopular acquisition)

2. Sector-wide (e.g. supply chain disruptions)

3. Regulatory actions (e.g. tariff revisions)

4. Macroeconomic shifts (e.g. commodity price shocks)

Any of the above developments can trigger a special situation for a company and result in the mispricing of a company. The actual impact, however, varies meaningfully across companies, depending on differences in business models, balance‑sheet strength, market positioning, and their ability to adapt. The opportunity to invest, however, lies in identifying those companies where underlying fundamentals remain strong, and the price dislocation reflects temporary uncertainty rather than a structural deterioration in business quality.

Spotting the opportunity

At the start of 2019, one of India’s largest conventional power producers was facing challenging times owing to regulatory overhang, difficult business conditions, and weaker performance on key operating parameters. The situation deteriorated significantly with the onset of the COVID-19 pandemic. Tightening of financing options even for mildly stressed power plants was a negative development. Under such circumstances, the market undermined the value offered by one of the India’s largest power producing companies. The valuation discount offered immense comfort. The company not only survived the challenging phase but also outlined a multi-year growth path that emphasized the importance of non-fossil energy.

As stated earlier, special situations can arise from both company-specific and sector-wide developments. For example, an unpopular large acquisition may trigger a sharp de-rating of a company, presenting an entry opportunity. When faced with such situations, the company’s management track record in integrating businesses becomes crucial. Additionally, even if traditional valuation metrics appear stretched, a strong strategic rationale and growth potential can offer a compelling margin of safety.

Similarly, sector consolidation presents opportunities. Prior to the pandemic, India’s telecom industry was beset by intense competition, high capital expenditures, and price wars. Over the years, only the strongest players survived. As the sector gradually evolved into a duopoly, it became increasingly clear that the Average Revenue Per User (ARPU) would likely rise, driven by structural factors. This shift resulted in a multi-year re-rating of the sector. While this may appear to be a classic case of re-rating-led value investing, the differentiating factor was that the growth potential of the sector seemed to have been overlooked under changing circumstances.

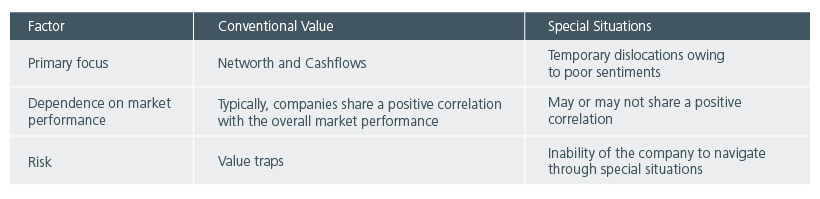

Fig 1: How special situations differ from conventional value investing?

Source: ICICI Prudential Asset Management Company Ltd (IPAMC)

Evaluating payoffs in special situations

Evaluating an investment’s potential payoff is key to portfolio construction. It involves assessing the conditions under which returns may materialise in the foreseeable future, helping portfolio managers allocate capital effectively and manage risk. While standard investments focus on predictable growth and fundamentals, special situations require a different lens, one that identifies temporary dislocations and mispricings.

In the case of a special situation, the focus is primarily on two factors:

1) Can companies effectively navigate through special situations?

2) Have valuations and prices corrected adequately to offer a meaningful upside from the estimated intrinsic values?

In other words, the portfolio manager must evaluate the overall nature of the special situations while also estimating the upside potential of the company as these situations unfold. The nature of a special situation could be complex or simple. Similarly, there can be more than one special situation present at a given point. Assessing the ability of the company’s management team to navigate challenging situations is a qualitative aspect of special situations investing, requiring years of in-depth analysis to grasp the nuances behind management decisions.

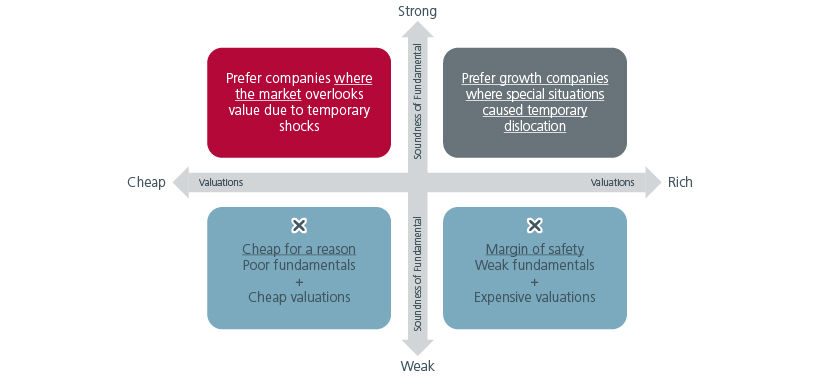

Fig 2: Special situations payoff vs. preferences grid

Source: ICICI Prudential Asset Management Company Ltd (IPAMC)

Why India presents a compelling case for special situations?

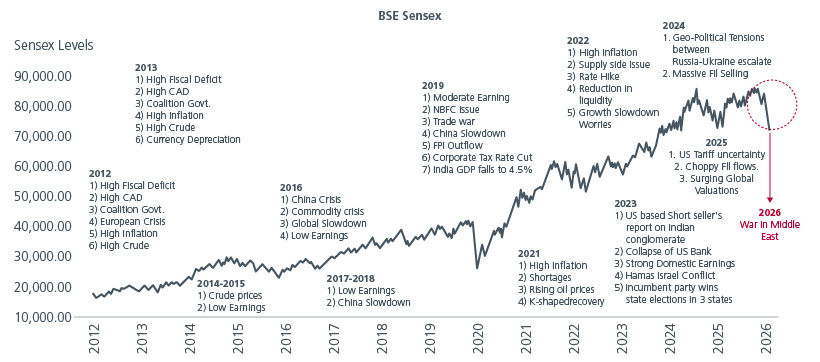

Special situations are not unique to India and are globally referred to as event‑driven investing. Indian markets have experienced numerous episodes of disruption repeatedly over time. This recurring pattern highlights that periods of heightened uncertainty are a recurring feature rather than isolated events.

Fig 3: Episodes of disruption

Source: BSE as of 31 March 2026. CAD- Current Account Deficit, NBFC- Non-Banking Financial Company, FPI- Foreign Portfolio Investment. GDP – Gross Domestic Product, Covid- Corona virus Disease.

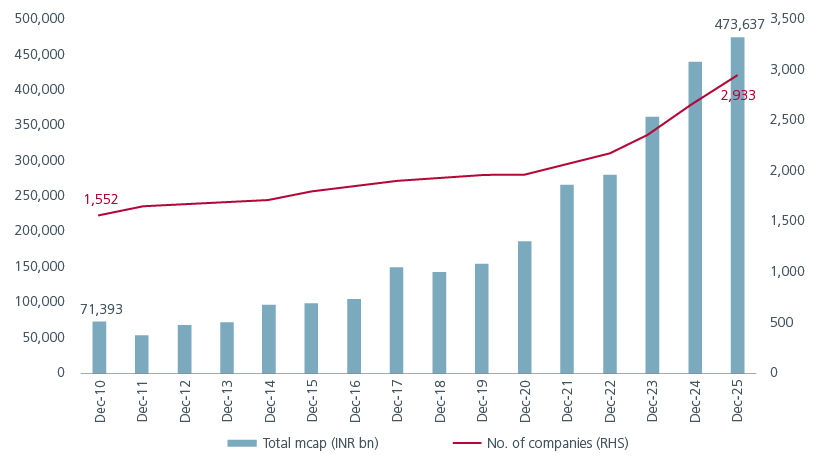

Furthermore, India offers a materially larger opportunity set; it is one of the most diversified and liquid markets globally, particularly within Asia, with over 2,900 listed companies having a total collective market cap of over USD 5 tn as of December 31, 2025.1 Over the last 15 years, India’s market cap has witnessed a 7x growth while the number of companies listed on the National Stock Exchange (NSE) have nearly doubled2. In 2018, the market cap of India’s smallest large cap i.e. that of the 100th largest company by market cap was ~INR 293 bn; at present, India’s top 250 companies individually have market capitalisation higher than INR 300 bn3.

Fig 4: Progress of Indian Market

Source: Jefferies as of 6 March 2026

Rising uncertainties due to changing geopolitical equations, the resilience of fundamentals, a unique (promoter-driven) shareholding structure, and the dynamic nature of the listed universe make India one of the uniquely positioned markets to scout for special situations.

Identifying special situations that have the potential to create alpha is a skilled task that requires a thorough understanding of both qualitative and quantitative aspects associated with these situations, as well as the companies involved. Outsized reactions create the potential for outsized returns.

This article was contributed by ICICI Prudential Asset Management Company Ltd

Interesting reads

Sources:

1 Jefferies, Dec 2025

2 Jefferies, Mar 2026

3 AMFI, Dec 2025

Singapore by Eastspring Investments (Singapore) Limited (UEN: 199407631H)

Australia (for wholesale clients only) by Eastspring Investments (Singapore) Limited (UEN: 199407631H), which is incorporated in Singapore, is exempt from the requirement to hold an Australian financial services licence and is licensed and regulated by the Monetary Authority of Singapore under Singapore laws which differ from Australian laws

Hong Kong by Eastspring Investments (Hong Kong) Limited and has not been reviewed by the Securities and Futures Commission of Hong Kong.

Indonesia by PT Eastspring Investments Indonesia, an investment manager that is licensed, registered and supervised by the Indonesia Financial Services Authority (OJK).

Malaysia by Eastspring Investments Berhad (200001028634/ 531241-U) and Eastspring Al-Wara’ Investments Berhad (200901017585 / 860682-K) and has not been reviewed by Securities Commission of Malaysia.

Thailand by Eastspring Asset Management (Thailand) Co., Ltd.

United States of America (for institutional clients only) by Eastspring Investments (Singapore) Limited (UEN: 199407631H), which is incorporated in Singapore and is registered with the U.S Securities and Exchange Commission as a registered investment adviser.

European Economic Area (for professional clients only) and Switzerland (for qualified investors only) by Eastspring Investments (Luxembourg) S.A., 26, Boulevard Royal, 2449 Luxembourg, Grand-Duchy of Luxembourg, registered with the Registre de Commerce et des Sociétés (Luxembourg), Register No B 173737.

Chile (for institutional clients only) by Eastspring Investments (Singapore) Limited (UEN: 199407631H), which is incorporated in Singapore and is licensed and regulated by the Monetary Authority of Singapore under Singapore laws which differ from Chilean laws.

The afore-mentioned entities are hereinafter collectively referred to as Eastspring Investments.

The views and opinions contained herein are those of the author, and may not necessarily represent views expressed or reflected in other Eastspring Investments’ communications. This document is solely for information purposes and does not have any regard to the specific investment objective, financial situation and/or particular needs of any specific persons who may receive this document. This document is not intended as an offer, a solicitation of offer or a recommendation, to deal in shares of securities or any financial instruments. It may not be published, circulated, reproduced or distributed without the prior written consent of Eastspring Investments. Reliance upon information in this document is at the sole discretion of the reader. Please carefully study the related information and/or consult your own professional adviser before investing.

Investment involves risks. Past performance of and the predictions, projections, or forecasts on the economy, securities markets or the economic trends of the markets are not necessarily indicative of the future or likely performance of Eastspring Investments or any of the funds managed by Eastspring Investments.

Information herein is believed to be reliable at time of publication. Data from third party sources may have been used in the preparation of this material and Eastspring Investments has not independently verified, validated or audited such data. Where lawfully permitted, Eastspring Investments does not warrant its completeness or accuracy and is not responsible for error of facts or opinion nor shall be liable for damages arising out of any person’s reliance upon this information. Any opinion or estimate contained in this document may subject to change without notice.

Eastspring Investments companies (excluding joint venture companies) are ultimately wholly owned/indirect subsidiaries of Prudential plc of the United Kingdom. Eastspring Investments companies (including joint venture companies) and Prudential plc are not affiliated in any manner with Prudential Financial, Inc., a company whose principal place of business is in the United States of America or with the Prudential Assurance Company Limited, a subsidiary of M&G plc (a company incorporated in the United Kingdom).