Rong Ren Goh

Portfolio Manager, Head of Macro and Thematics,

Asian Fixed Income,

Eastspring Investments

Mar 2026|5 min read

Executive Summary

- Asian bonds have remained relatively resilient compared to US and European bonds amid the recent geopolitical developments.

- Asia’s macro fundamentals have improved while many Developed Markets are experiencing high fiscal deficits and rising government debt.

- Asian bonds’ lower correlations with global bond markets during periods of market stress and still-competitive long-term returns can help improve risk‑adjusted outcomes in portfolios.

Following recent geopolitical developments, risk assets have sold off, global bond yields have moved higher to price in the inflationary impact of rising oil prices and credit spreads have widened. Yet, Asian bonds have remained relatively resilient to date, with the JP Morgan Asian Credit Index (JACI) down less than 1% year to date1. Part of this resilience, we believe, comes from Asia’s improving long-term macro fundamentals.

Investors have traditionally turned to Developed Market (DM) bonds as a key source of income. In seeking stable and predictable cash flows, income investors have viewed DM bonds as offering greater stability, credible policy frameworks, stable currencies and more durable real returns. However, this long‑held narrative has begun to shift. Asian bonds are exhibiting greater resilience as volatility rises in DM bonds.

When developed market bonds test long-held assumptions

In recent years, a pattern has emerged in which policy missteps and fiscal uncertainty have triggered weakness in both DM currencies and bonds. In November 2025 for example, the yields of UK gilts and Japanese government bonds rose sharply on the back of fiscal concerns while their currencies slipped. In the UK, the pressure came after the government signalled that planned tax increases may be rolled back, raising questions over the UK’s fiscal trajectory. In Japan, a larger than expected supplementary budget under Prime Minister Takaichi prompted a similar market response.

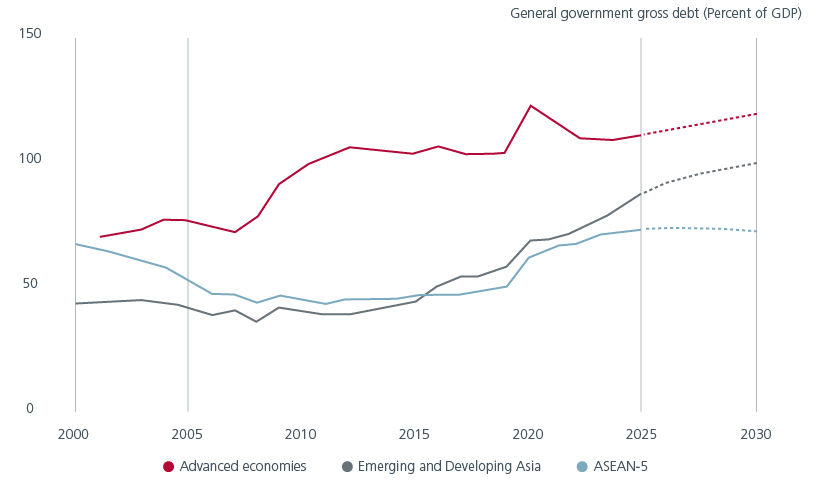

Many DMs are experiencing high fiscal deficits and rising government debt with limited political capital for fiscal consolidation. Fig. 1. When spending cuts and tax hikes are off the table and default is not an option, inflation and currency depreciation become the path of adjustment. This dynamic that used to be part of the risks associated with investing in Emerging Markets is now appearing in DMs.

Fig. 1. Advanced economies have higher government debt levels

Source: World Economic Outlook. October 2025.

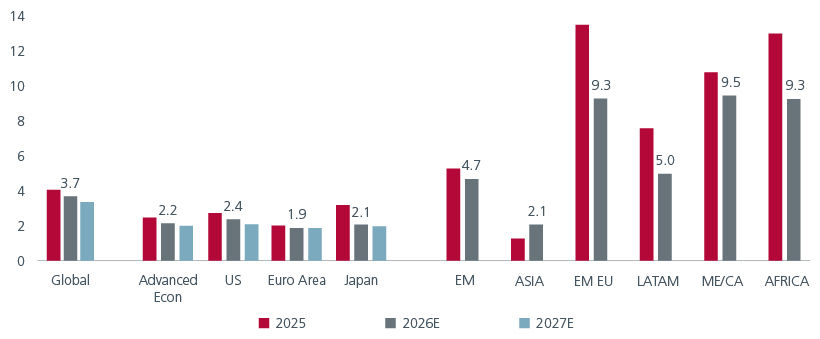

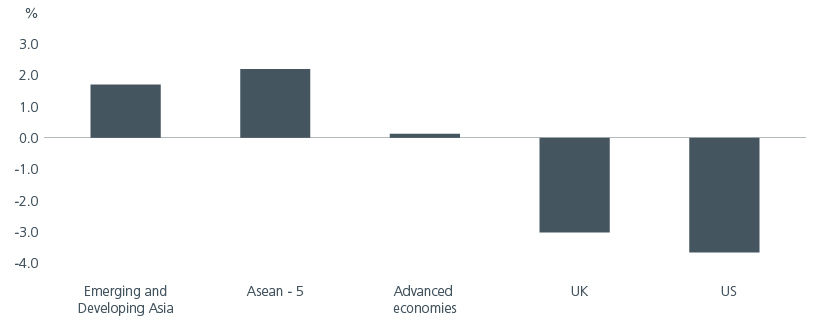

On the other hand, in Emerging Asia, fiscal discipline has been steadier, and inflation better contained. Fig. 2. Policy credibility remains largely intact and real yields are positive for the right reasons. External balances are also healthier and domestic savings in the region continue to rise. Fig. 3. In the recent Middle East conflict, the current account surpluses in many Asian economies can provide some cushion to absorb higher energy costs. Meanwhile parts of Asia continue to benefit from the strong demand for AI-related exports.

Fig. 2. Headline inflation in Asia has been contained

Source: IMF staff estimates. Eastspring Investments. Jan 2026. E=Expected. Any projection or forecast is not necessarily indicative of the future or likely performance. Legend: Global – World. Advanced Econ – G3 (US, Eurozone, Japan). EM – Emerging Europe. LATAM – Latin America. ME/CA – Middle East/Central Asia.

Fig. 3. 2025 Current account balances (% of GDP) in Asia looks healthy

Source: IMF datamapper. Extracted on 27 February 2026. 2025 data or latest available data shown.

Although geopolitical tensions may be supportive of the USD in the near term, the dollar appears overvalued on several measures including the REER (Real Effective Exchange Rate). The US’ Net International Investment Position (NIIP) is also at its most negative level since 1975. A negative NIIP means that the foreign claims on US assets are larger than the US’ claims abroad. This extended position makes the USD potentially vulnerable and biased lower should foreign investors seek to diversify their investments and foreign reserves away from USD assets, after reassessing the US’ fiscal sustainability.

Resilience without sacrificing returns

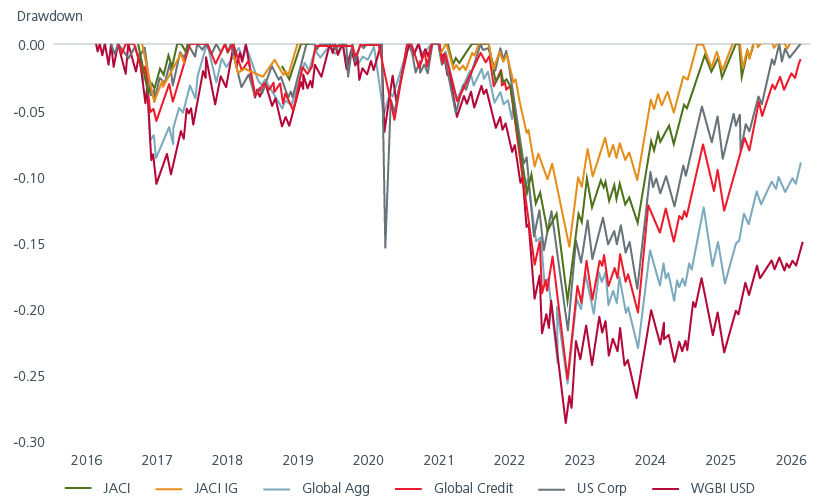

Asian USD bonds have been able to show greater resilience during periods of market stress. This was seen during the 2022 global rates and credit sell-off, when aggressive global monetary tightening drove deep and simultaneous losses across many traditional defensive assets. Compared to global credit and government bond markets, Asian USD bonds experienced smaller peak-to-trough declines and, importantly, recovered more quickly as market conditions stabilised. Fig. 4. In the recent Iran war, Asian Investment Grade (IG) bonds have also outperformed US and European IG bonds2 month to date.

Fig. 4. Asian bonds experienced lower drawdowns in 2022

Source: Bloomberg, Feb 2026.

We have also seen correlations between Asian credit and global bond markets decline during periods of heightened stress. This differentiated behaviour can help cushion portfolios during global risk-off episodes. Fig. 5.

Fig. 5. Correlation between Asian credit and global bond markets fall during periods of market stress

Source: Bloomberg, Feb 2026. Rolling 1-year correlation vs JACI.

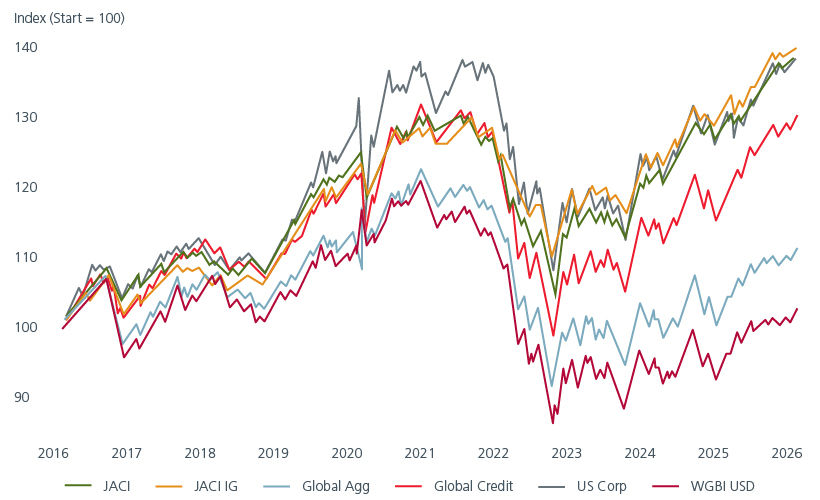

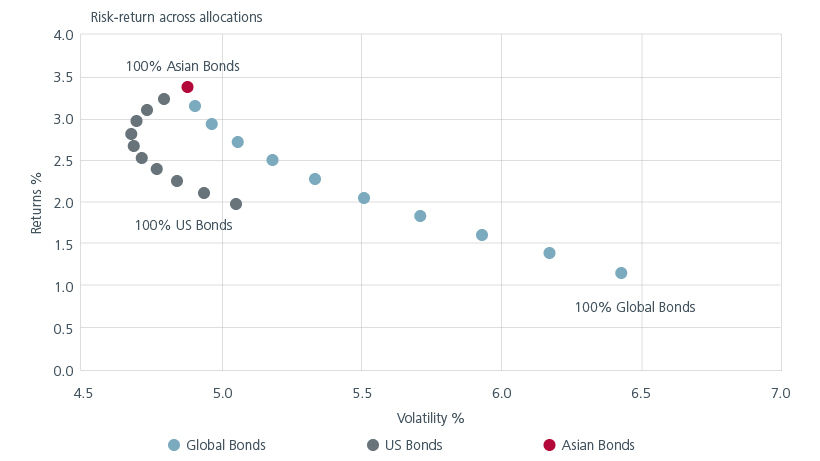

Not only are Asian bonds more resilient, historically, but they have also delivered competitive long-term returns. Fig. 6. This combination is increasingly valuable as global bond markets come under pressure from sharp interest rate repricing, tighter financial conditions and periods of risk aversion. Fig. 7 shows that based on 10-year returns, adding Asian bonds to a portfolio of US or global bonds can improve the risk-return balance.

Fig. 6. Asian bonds have delivered competitive long-term returns

Source: Bloomberg, Feb 2026. Rebased to 100 from 2016.

Fig. 7. Adding Asian bonds can improve portfolio’s risk-return balance

Source: Eastspring Investments. Bloomberg. Asian Bonds – JACI. US Bonds – US Aggregate. Global Bonds – Global Aggregate.

Asia’s rising role in income portfolios

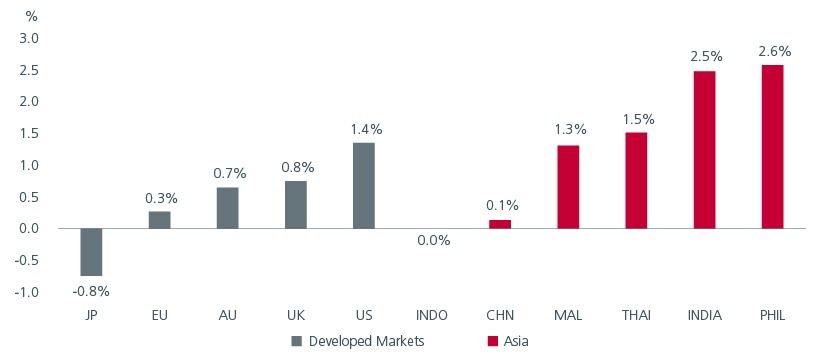

The growing resilience of Asian bond markets means that Asian bonds are increasingly relevant as a core allocation within income portfolios. For long-term income investors seeking credible policy anchors and durable real returns, Asian bonds stand out as a compelling opportunity, offering diversification benefits alongside attractive real yields. Fig. 8.

Fig.8. Asia offers higher real yields than developed markets

Source : Bloomberg, 10 March 2026.

In an environment marked by geopolitical tensions, policy uncertainty and shifting macro regimes, flexible bond strategies that can access both USD and local currency bond markets, as well as manage currencies dynamically, are likely to have an advantage. An active approach that navigates Asia’s diverse macroeconomic and credit fundamentals, along with differing monetary, fiscal and local market dynamics, can help investors capture income opportunities and enhance portfolio resilience, especially when it matters most.

Interesting reads

Sources:

1 Bloomberg. As of 25 March 2026.

2 Bloomberg. In USD terms. As of 26 March 2026.

Singapore by Eastspring Investments (Singapore) Limited (UEN: 199407631H)

Australia (for wholesale clients only) by Eastspring Investments (Singapore) Limited (UEN: 199407631H), which is incorporated in Singapore, is exempt from the requirement to hold an Australian financial services licence and is licensed and regulated by the Monetary Authority of Singapore under Singapore laws which differ from Australian laws

Hong Kong by Eastspring Investments (Hong Kong) Limited and has not been reviewed by the Securities and Futures Commission of Hong Kong.

Indonesia by PT Eastspring Investments Indonesia, an investment manager that is licensed, registered and supervised by the Indonesia Financial Services Authority (OJK).

Malaysia by Eastspring Investments Berhad (200001028634/ 531241-U) and Eastspring Al-Wara’ Investments Berhad (200901017585 / 860682-K) and has not been reviewed by Securities Commission of Malaysia.

Thailand by Eastspring Asset Management (Thailand) Co., Ltd.

United States of America (for institutional clients only) by Eastspring Investments (Singapore) Limited (UEN: 199407631H), which is incorporated in Singapore and is registered with the U.S Securities and Exchange Commission as a registered investment adviser.

European Economic Area (for professional clients only) and Switzerland (for qualified investors only) by Eastspring Investments (Luxembourg) S.A., 26, Boulevard Royal, 2449 Luxembourg, Grand-Duchy of Luxembourg, registered with the Registre de Commerce et des Sociétés (Luxembourg), Register No B 173737.

Chile (for institutional clients only) by Eastspring Investments (Singapore) Limited (UEN: 199407631H), which is incorporated in Singapore and is licensed and regulated by the Monetary Authority of Singapore under Singapore laws which differ from Chilean laws.

The afore-mentioned entities are hereinafter collectively referred to as Eastspring Investments.

The views and opinions contained herein are those of the author, and may not necessarily represent views expressed or reflected in other Eastspring Investments’ communications. This document is solely for information purposes and does not have any regard to the specific investment objective, financial situation and/or particular needs of any specific persons who may receive this document. This document is not intended as an offer, a solicitation of offer or a recommendation, to deal in shares of securities or any financial instruments. It may not be published, circulated, reproduced or distributed without the prior written consent of Eastspring Investments. Reliance upon information in this document is at the sole discretion of the reader. Please carefully study the related information and/or consult your own professional adviser before investing.

Investment involves risks. Past performance of and the predictions, projections, or forecasts on the economy, securities markets or the economic trends of the markets are not necessarily indicative of the future or likely performance of Eastspring Investments or any of the funds managed by Eastspring Investments.

Information herein is believed to be reliable at time of publication. Data from third party sources may have been used in the preparation of this material and Eastspring Investments has not independently verified, validated or audited such data. Where lawfully permitted, Eastspring Investments does not warrant its completeness or accuracy and is not responsible for error of facts or opinion nor shall be liable for damages arising out of any person’s reliance upon this information. Any opinion or estimate contained in this document may subject to change without notice.

Eastspring Investments companies (excluding joint venture companies) are ultimately wholly owned/indirect subsidiaries of Prudential plc of the United Kingdom. Eastspring Investments companies (including joint venture companies) and Prudential plc are not affiliated in any manner with Prudential Financial, Inc., a company whose principal place of business is in the United States of America or with the Prudential Assurance Company Limited, a subsidiary of M&G plc (a company incorporated in the United Kingdom).