Rong Ren Goh

Portfolio Manager, Head of Macro and Thematics,

Asian Fixed Income,

Eastspring Investments

June 2026|5 min read

Clement Chong

Head of Credit Research, Fixed Income,

Eastspring Investments

Executive Summary

- We are focused on generating resilient carry for portfolios and look to extend duration when we have greater conviction that inflation and interest rates have peaked.

- The diverse outlook for Asian currencies would impact Asian local currency bond returns. We prefer economies that have stronger balance of payment positions including SGD and AUD.

- Asian credits begin from a position of strength, with the largely investment-grade JACI APAC universe well placed to navigate a higher inflation, slower growth environment.

US 10-year Treasury bond yields have risen more than 50 bps from their 2026 low as concerns over inflation mount1. Against this backdrop, Asian bonds, measured by the JACI Composite Total Return Index, is still marginally positive for the year (+0.8%), outperforming global bonds (+0.1%)2.

1. With the recent sell-off in bond yields, do you see this as an opportunity to add duration?

Rong Ren: We remain cautious on adding duration even after the recent rise in yields, as data over the coming months is likely to reflect stronger inflationary pressures. Besides higher energy prices, food prices are also expected to rise because of higher fertiliser prices - an estimated 30–35% of global fertiliser trade moves through the Strait of Hormuz. This could keep yields elevated.

In Asia, the policy narrative has shifted from rate cuts in 2025 to a bias of either keeping rates on hold or hiking rates in 2026. Selected Asian central banks may consider rate hikes following recent currency weakness. In the US, while the market is currently pricing in hikes of 20 bp for the rest of 2026, and 30bp for 20273, the rate outlook remains uncertain given the evolving inflation outlook.

A sustained bond market rally would likely require a more prolonged focus on weakening global growth. That said, a near-term relief rally could emerge if there is a quick resolution to the Middle East conflict. In such a scenario, investors may look through the near-term inflationary impulse - crude shipping volumes would take several months to normalise even if the Strait of Hormuz is reopened.

Against this backdrop, we remain neutral and tactical on duration rather than underweight. We would look to extend duration when we have greater conviction that inflation and interest rates have peaked.

2. Where do you see the potential opportunities and risks in the Asian local currency bond market?

Rong Ren: Value has emerged as Asian local currency rates and currencies sold off in May. Nevertheless, we remain highly selective give the diverse currency outlooks across the region. With higher energy prices likely to impact inflation and economic activity, policy trade-offs will become harder. As such, economies with stronger balance of payments positions should fare better.

I like AUD bonds for their attractive carry. The Reserve Bank of Australia has been one of the more hawkish central banks in the region in 2026, even as many Asian peers remained on hold or eased. Meanwhile, SGD bonds, as measured by the Markit iBoxx ALBI Singapore Total Return Index, is up 3.0% year to date4. SGD bonds should continue to benefit from the currency’s safe-haven status and the economy’s relative resilience. The corporate supply backdrop remains constructive, despite a recent uptick in bank issuance. This should help support the SGD credit market. Longer term Thai sovereigns also present an interesting opportunity as the Bank of Thailand is unlikely to hike rates given the country’s weak economic outlook. In addition, the broadening of the artificial intelligence (AI) capital expenditure (capex) cycle should support the KRW and TWD.

On the other hand, I am more cautious on the currency outlook for the high yielders (Indian Rupee, Indonesian Rupiah and Philippines Peso). High energy prices are likely to further weaken their balance of payments positions. In addition, the stock markets in these countries do not benefit from the prevailing AI investment theme, which could otherwise have attracted foreign portfolio inflows supportive of their currencies.

3. What has been the impact of higher energy prices on credit quality in Asia?

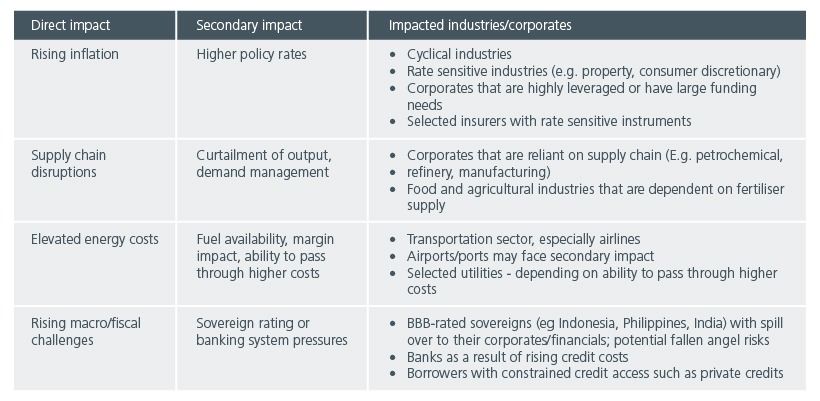

Clement: Asian high yield bonds have outperformed their US peers on a year-to-date basis while Asian investment grade bonds have performed largely in line with US investment grade bonds5. The fundamental picture for Asian corporates still looks relatively healthy. Admittedly, more companies are turning cautious and the extent of the impact will hinge on the duration of the Middle East conflict. With manufacturers experiencing longer delivery times and higher input costs, we may start to see more negative earnings revisions as margins come under pressure. This would pressure earnings rather than balance sheets, with varying degrees of impact across industries. Fig. 1.

Fig. 1. Transmission mechanism of higher energy prices in Asia

Source: Eastspring Investments. May 2026.

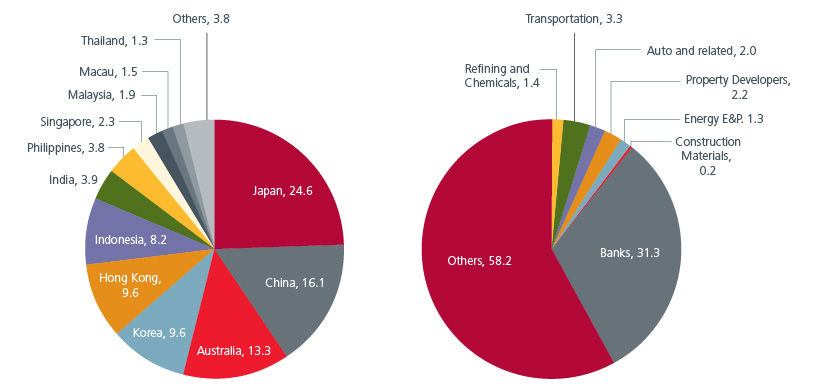

One mitigating factor is that Asian corporates are coming from a position of strength. Credit metrics such as Debt/EBITDA remain relatively healthy for investment grade credits and is stable for high yield credits. Credit rating momentum to date has also been fairly balanced between upgrades and downgrades. While we are more cautious on the macro outlook for India, Indonesia and Philippines, the rest of Asia appears fairly resilient. Likewise for industries: while the refining, transportation and auto sectors are more vulnerable to higher energy prices and supply chain disruptions, the other industries are likely to weather through this challenging period. Fig. 2. The JACI APAC benchmark is predominantly an investment grade universe, and we believe that the proportion of sovereigns or industries that are sensitive to these challenges is manageable. That said, it is important to remain highly selective as credit spreads remain tight.

Fig. 2. Breakdown of JACI APAC(%)

Source: JACI APAC Index. 14 May 2026.

4. How are you positioning portfolios in the current environment?

Rong Ren: We remain focused on generating resilient carry for the portfolio while maintaining discipline around credit quality, liquidity and downside risk.

Within credit, we continue to look for opportunities to add selectively to issuers where spreads have widened due to technical factors rather than any deterioration in fundamentals. Security selection is key as performance gains have been narrow and concentrated.

Risk management and agility are also important in navigating any potential subsequent shocks. We need to manage duration appropriately to address the upcoming inflation shock and reassess when to extend duration when the growth shock becomes more prominent.

Interesting reads

Sources:

1 Bloomberg as of 1 June 2026.

2 Bloomberg as of 2 June 2026. In USD terms. Global bonds proxied by the Bloomberg Global Aggregate Total Return Index.

3 Bloomberg as of 22 May 2026.

4 Bloomberg as of 2 June. In USD terms.

5 Bloomberg.

As of 29 May 2026.

Singapore by Eastspring Investments (Singapore) Limited (UEN: 199407631H)

Australia (for wholesale clients only) by Eastspring Investments (Singapore) Limited (UEN: 199407631H), which is incorporated in Singapore, is exempt from the requirement to hold an Australian financial services licence and is licensed and regulated by the Monetary Authority of Singapore under Singapore laws which differ from Australian laws

Hong Kong by Eastspring Investments (Hong Kong) Limited and has not been reviewed by the Securities and Futures Commission of Hong Kong.

Indonesia by PT Eastspring Investments Indonesia, an investment manager that is licensed, registered and supervised by the Indonesia Financial Services Authority (OJK).

Malaysia by Eastspring Investments Berhad (200001028634/ 531241-U) and Eastspring Al-Wara’ Investments Berhad (200901017585 / 860682-K).

Thailand by Eastspring Asset Management (Thailand) Co., Ltd.

United States of America (for institutional clients only) by Eastspring Investments (Singapore) Limited (UEN: 199407631H), which is incorporated in Singapore and is registered with the U.S Securities and Exchange Commission as a registered investment adviser.

European Economic Area (for professional clients only) and Switzerland (for qualified investors only) by Eastspring Investments (Luxembourg) S.A., 26, Boulevard Royal, 2449 Luxembourg, Grand-Duchy of Luxembourg, registered with the Registre de Commerce et des Sociétés (Luxembourg), Register No B 173737.

Chile (for institutional clients only) by Eastspring Investments (Singapore) Limited (UEN: 199407631H), which is incorporated in Singapore and is licensed and regulated by the Monetary Authority of Singapore under Singapore laws which differ from Chilean laws.

The afore-mentioned entities are hereinafter collectively referred to as Eastspring Investments.

The views and opinions contained herein are those of the author, and may not necessarily represent views expressed or reflected in other Eastspring Investments’ communications. This document is solely for information purposes and does not have any regard to the specific investment objective, financial situation and/or particular needs of any specific persons who may receive this document. This document is not intended as an offer, a solicitation of offer or a recommendation, to deal in shares of securities or any financial instruments. It may not be published, circulated, reproduced or distributed without the prior written consent of Eastspring Investments. Reliance upon information in this document is at the sole discretion of the reader. Please carefully study the related information and/or consult your own professional adviser before investing.

Investment involves risks. Past performance of and the predictions, projections, or forecasts on the economy, securities markets or the economic trends of the markets are not necessarily indicative of the future or likely performance of Eastspring Investments or any of the funds managed by Eastspring Investments.

Information herein is believed to be reliable at time of publication. Data from third party sources may have been used in the preparation of this material and Eastspring Investments has not independently verified, validated or audited such data. Where lawfully permitted, Eastspring Investments does not warrant its completeness or accuracy and is not responsible for error of facts or opinion nor shall be liable for damages arising out of any person’s reliance upon this information. Any opinion or estimate contained in this document may subject to change without notice.

Eastspring Investments companies (excluding joint venture companies) are ultimately wholly owned/indirect subsidiaries of Prudential plc of the United Kingdom. Eastspring Investments companies (including joint venture companies) and Prudential plc are not affiliated in any manner with Prudential Financial, Inc., a company whose principal place of business is in the United States of America or with the Prudential Assurance Company Limited, a subsidiary of M&G plc (a company incorporated in the United Kingdom).